The insurance industry is at a crossroads when it comes to managing claims. A staggering 80 cents of every dollar earned on premiums is typically funneled into claims, which highlights the growing pressure insurers face to improve their claims processes. But cost isn’t the only reason insurers should prioritize transforming their claims operations: The claims experience remains a vital touchpoint between insurers and their customers.

Unfortunately, it’s also the source of the majority of consumer complaints in the industry, 70.9%, in fact, reflecting a significant opportunity for improvement. Claims management is one of the most important levers for insurers to generate value and strengthen customer relationships. As the insurance ecosystem continues to evolve, transforming the claims value chain is no longer optional — it’s imperative for staying competitive.

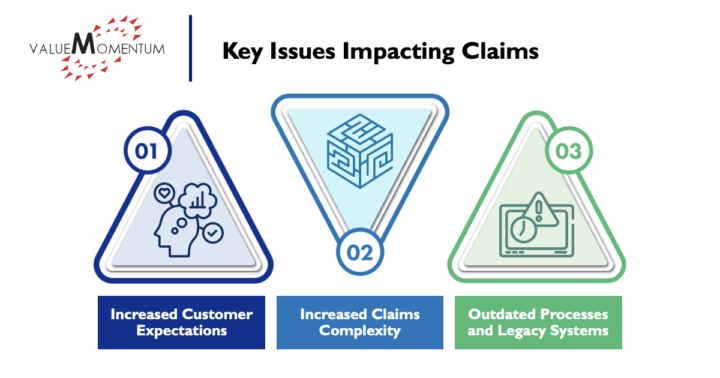

The Current State of Claims

The insurance industry is grappling with a growing disconnect between customer expectations and the current state of claims management. Between the need for more digital experiences, growing threats within the insurance industry, and a reliance on legacy systems and manual processes, the current state of claims is on the brink of making or breaking insurers.

Here is how each of these key issues is impacting today’s claims experience:

Increased Expectations for Customer Experience

Customers are demanding more personalized, seamless experiences across every industry — and insurance is no exception. When it comes to submitting a claim and tracking its status, policyholders expect a modern, omnichannel claims experience that balances digital elements with human interactions.

In addition, many prefer a self-service experience, with 19% of insurance customers churning due to a lack of self-service options. Consumers want transparent, real-time communication throughout the entire process, as well as greater visibility into the status of their claims.

Unfortunately, many insurers are still struggling to deliver this level of service, relying on outdated systems and manual processes that slow down resolution times and frustrate customers.

Increased Complexity in Claims

In addition to heightened customer expectations, the complexity of claims has increased significantly in recent years.

The rise in natural disasters and large-scale catastrophes has led to a surge in claims volume, often requiring more intricate handling and longer processing times. Swiss RE found total insured losses from natural disasters climbed past $122 billion worldwide. On top of this, claims fraud is becoming increasingly sophisticated, leading to a higher frequency of fraudulent claims and greater scrutiny in processing each case. The propensity for litigation in claims has also increased, making claims management more complex than ever.

This complexity translates to longer cycle times, higher payouts, and more claims leakage, further eroding insurers’ profitability and consumers’ trust.

Outdated Processes and Legacy Systems

Another critical issue is the prevalence of outdated claims processes and legacy systems. While many insurers have upgraded their platforms, the underlying practices remain rooted in old, manual ways of doing things.

For example, although claims handling is done on newer platforms, it still requires human intervention at every step of the process. Even in cases where digital platforms are used, the processes themselves may not have been updated, or there is a lack of integration between systems, resulting in inefficiency and errors. This combination of outdated processes and systems leads to higher costs, delays, and missed opportunities for improvement. As a result, insurers face mounting pressure to modernize their claims operations to keep up with the evolving landscape.

These factors all make it harder — and make it take longer — to resolve claims, ultimately affecting customer satisfaction and insurers’ bottom lines.

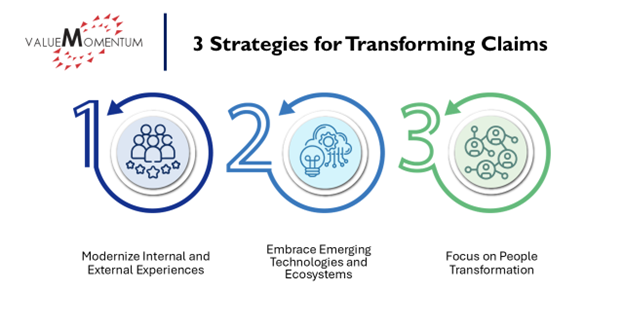

Transforming Insurance Claims: Three Strategic Imperatives for Insurers

While many insurers have taken steps to upgrade their platforms, there’s still much work to be done to truly transform internal operations and customer interactions.

Here are three key strategies to drive meaningful change in the claims landscape.

1. Modernize Internal and External Experiences

While many insurers have made strides by upgrading their claims management platforms, they still rely on outdated processes for claims handling, communication, and data sharing. Manual workflows create inefficiencies, delay resolutions, and negatively impact customer satisfaction.

To remain competitive, insurers must go beyond upgrading technology platforms — they need to redefine and transform their underlying processes. This means streamlining internal workflows, automating routine tasks, and enhancing the customer journey from claim submission to payout.

By improving both internal operations and customer-facing touchpoints, insurers can reduce costs, accelerate claims processing, and deliver a seamless, frictionless experience that meets evolving customer expectations.

2. Embrace Emerging Technologies and Ecosystems

Insurers who fail to leverage emerging technologies and new ecosystems risk being left behind. The rise of technologies like artificial intelligence (AI), generative AI (GenAI), machine learning, and IoT is reshaping the way claims can be processed and managed. Insurers have a significant opportunity to use these technologies to innovate and stay ahead.

In addition, insurtech companies and ecosystems specializing in specific claims processes — such as fraud detection, straight-through processing, low-touch claims, and document processing — offer valuable opportunities for integration. Partnering with organizations who can help insurers integrate these ecosystems and emerging technologies into their claims landscape can unlock efficiencies, reduce manual effort, and increase overall value.

For example, AI can be used to assess claims more accurately and quickly, while IoT devices can provide real-time data to help prevent claims from occurring in the first place. By embracing these technologies, insurers can streamline their processes, reduce fraud, and improve the overall claims experience for customers.

3. Focus on People Transformation

Behind every successful claim process, there are skilled claims adjusters who handle complex cases and engage directly with customers. However, many insurers are facing a growing skills gap as experienced adjusters retire and younger professionals enter the workforce. Protecting institutional knowledge and ensuring that new adjusters are equipped with the right skills is crucial for maintaining the quality of claims handling.

Insurers should focus on continuous training and development programs that equip adjusters with advanced communication, data analysis, and customer engagement skills. By transforming the role of adjusters from process-oriented operators to customer-focused advisors, insurers can not only improve the claims experience but also foster long-term customer loyalty.

Driving the Future of Claims

As customer expectations continue to rise and claims grow more complex, the future of insurance claims depends on the seamless integration of technology, process optimization, and people transformation. Insurers have an opportunity to move beyond incremental improvements and create a transformative impact by reimagining the role of their claims departments.

By modernizing experiences, adopting cutting-edge technologies, and strategically investing in talent, insurers can significantly improve operational efficiency, enhance customer trust, and foster loyalty. More importantly, they can shift their claims function from being a reactive back-office cost center to a proactive, value-generating powerhouse.

The time to act is now. Insurers that adopt these strategies will not only redefine the claims experience but also position themselves as leaders in shaping the future of the industry. A well-executed transformation can make claims a competitive advantage, unlocking new levels of customer satisfaction and long-term profitability.

Interested in learning more about how to improve the customer experience? Read our case study, “Multi-line Insurer Improves Customer Experience with SmartCOMM.”