Mobile apps have become the primary interface for managing daily life. According to Pew Research Center’s 2025 Mobile Fact Sheet, 91% of U.S. adults own a smartphone. People use their phones to check their bank balances, order groceries, schedule appointments, and receive medical test results. It is now a baseline expectation that any service worth using should be accessible, intuitive, and available on demand.

Insurance is not exempt. Policyholders already manage most of their financial and service relationships through mobile devices, and they increasingly bring those same expectations to interactions with their insurer. Yet many carriers have been slow to recognize the full strategic value of a mobile app, treating it as a convenient feature rather than a core component of the customer relationship.

As a result, the space between what consumers expect and what most insurance apps deliver is continuously widening. Closing that gap requires more than a functional app. It requires clarity about what role the app is meant to play and how to reach its full potential.

What Role Should a Mobile App for Insurance Play?

Before investing in app capabilities, carriers need to answer a foundational question: What value will this app provide our policyholders? The answer is not universal. Depending on a carrier’s distribution model, customer base, and strategic priorities, a mobile app can serve different functions. Understanding those functions clearly is the first step toward building something that delivers real value.

For carriers that sell through digital or direct channels, their mobile app often functions as the relationship itself. Consumers can get a quote, bind a policy, make a payment, and file a claim without ever speaking to a human. This model works well for standard, lower-complexity products, such as personal auto, renters insurance, and simple homeowners, where consumers are comfortable self-servicing and the transaction is relatively uncomplicated.

In an agent-distributed model, however, the dynamic shifts. The app’s role becomes one of support rather than a primary channel, handling routine, time-sensitive tasks that do not require human judgment: paying a bill, pulling up proof of insurance, checking a claim status, updating a mailing address.

By giving policyholders a self-service channel for these transactions, the app reduces inbound contact volume and frees agents to focus on higher-value interactions. The Insurity 2025 Digital Experience Index found that 48% of insurance consumers prefer a digital-first model that lets them handle simple transactions independently while providing the option to speak to someone when a more complex need emerges.

Beyond servicing, a well-designed app can also function as a growth tool. By monitoring a policyholder’s profile, life events, and coverage gaps, the app can surface cross-sell and upsell opportunities at the right moment — and hand the consumer off to an agent at the point of interest rather than waiting for the annual renewal conversation. A homeowner who just added a vehicle or a policyholder whose child just turned 16 represents an opening. The app identifies it; the agent closes it.

In practice, most carriers will find their app playing more than one of these roles. The more important question is not which role to choose, but how to build an app that serves all of them well. And that requires a different kind of framework altogether.

The Three A’s of a Customer-Centric Insurance App

Instead of thinking about app development as a series of feature decisions, carriers that build the most effective mobile experiences tend to think in terms of what the app should do for the customer at each stage of the relationship, and how the app can provide value beyond utility related to what they are insuring.

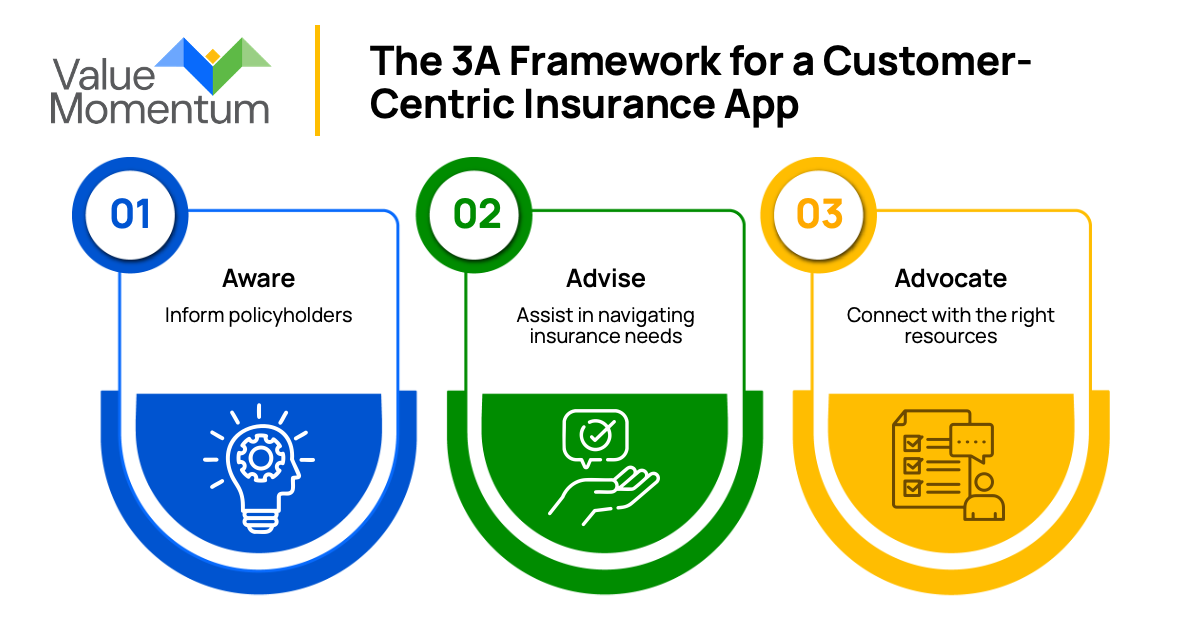

Three “A” functions — Aware, Advise, and Advocate — provide a useful framework for organizing that investment and for sequencing it in a way that builds toward long-term value.

1. Aware

The first job of any insurance app is to make the policyholder more informed. Insurance is a product most people interact with infrequently and understand imperfectly. They know they need it, they know it costs money, and they hope never to use it.

That dynamic creates a genuine opportunity for carriers willing to close the knowledge gap. An app that surfaces a quick explainer on what comprehensive coverage provides or that flags when a policyholder’s home valuation may no longer reflect replacement cost is adding value in a moment when the customer is not in crisis and can absorb it.

For agent-model carriers, this might take the form of short insurance literacy content, such as answering questions like, “What does liability coverage mean for you?” to educate the policyholder before they call an agent, making both interactions more productive. The goal at this stage is not to sell. It is to build the kind of informed relationship that makes every subsequent interaction easier.

2. Advise

Once a carrier has established a foundation of well-informed customers, the app can take on a more active role: helping the policyholder navigate their actual insurance needs. This is where utility becomes personal.

An app that detects the policyholder’s location and sends a weather alert ahead of a severe storm, prompting them to move their vehicle or document their property, is not just providing information. It is tending to their needs in real time based on what the carrier already knows about them: where they live, what they own, and what they are exposed to.

“Advise” also covers the transactional: helping a policyholder find a tow truck after a breakdown, walking them through a first notice of loss, or surfacing the right coverage option when life circumstances change. The common thread is the app is doing something useful for the customer, not asking something of them.

3. Advocate

The most mature expression of a mobile app is one that actively works on the policyholder’s behalf, anticipating needs before they are articulated, connecting them with the right resources at the right moment, and deepening the relationship over time.

This is where cross-sell and upsell live — framed not as commercial opportunities for the carrier, but as genuine recommendations for the customer. An app that recognizes a policyholder has recently had a child and surfaces a prompt to review their life coverage is doing advocacy work. So is an app that monitors renewal timing and puts the policyholder in touch with their agent before coverage lapses.

For agent-model carriers, the app does not replace conversation; it creates the conditions for it, arriving at the right moment with the right context so the agent can do what the app cannot: listen, advise, and build trust. The intelligence is in the app. The relationship is still with the person.

Carriers are unlikely to build toward all three stages at once, and they don’t need to. Most will start with utility, which means getting “Advise” right before moving toward “Advocate.” Having the full framework in view from the beginning, however, ensures early investments are made in a way that supports the app’s ultimate direction.

From Feature to Strategic Asset

Mobile apps represent one of the most direct but underutilized touchpoints a carrier has with its policyholders. Carriers that treat their app as a strategic asset rather than a digital checkbox are building something that compounds over time: each interaction that informs, assists, or advocates on the customer’s behalf deepens a relationship that is difficult for competitors to displace.

The three As framework is more than a product roadmap; it is a way of evaluating whether an app is earning its place in a policyholder’s daily life. An app that only processes transactions is doing the minimum. An app that raises awareness, tends to real needs, and advocates on behalf of the customer nurtures the relationship between carriers and their policyholders, ensuring that policyholders feel they can rely on their carrier in the moments when insurance is required.

For carriers ready to rethink what their mobile app for insurance can do, see how ValueMomentum helped a leading insurer reimagine its mobile customer experience and the business results that followed in our case study, “Leading Insurer Drives Mobile Customer Experience.”