Incorporating generative artificial intelligence (GenAI) in insurance is helping carriers reshape the way they conduct business across the value chain. GenAI is no longer just a matter of hype; according to McKinsey, AI could deliver the insurance industry up to $1.1 trillion in annual value globally.

Unlike traditional AI systems, which operate within predefined parameters, GenAI can generate novel outputs and content that have not been explicitly programmed. However, the cost of augmenting workflows with GenAI is substantial, from the initial investment required for infrastructure and training to the ongoing maintenance needed to keep the system at its best. But budgeting for these investments can pay off in the end; successfully leveraging GenAI capabilities can enable insurers to streamline their operations, improve overall efficiency, and ultimately reduce costs.

This blog post delves into the costs versus the financial benefits of GenAI in insurance as well as offers key strategies for measuring the success of GenAI implementations.

Where GenAI Pays Off for Insurers

By automating insurance process tasks, GenAI can streamline workflows and free up employees to spend their time on more strategic endeavors and places that truly require a human touch.

Take policy generation. Leveraging natural language processing and predefined templates, AI-powered systems can generate personalized policies swiftly and accurately, minimizing the risk of human error and expediting policy issuance. One smaller P&L insurer, for instance, is using a GenAI policy generation tool to create custom policies with personalized, dynamic premiums. As a result, the insurer saw a 10 percent uplift in operating profit.

On the claims side, claims processing often involves extensive documentation and manual verification. By automating data extraction and validation, GenAI-driven systems streamline the claims process, enabling faster and more accurate claim settlement. According to Boston Consulting Group, some insurers report productivity gains of up to 30 percent after using GenAI for claims processing.

In addition, GenAI can take the results of tools like chatbots and virtual assistants even further than previous AI-driven versions. Freshdesk found that customer satisfaction scores increased by 7 percent after the integration of chatbots. And by implementing GenAI in tasks like claims processing and policy generation, agents and employees are freed up to focus on customers with more critical needs that a chatbot wouldn’t be able to resolve.

The Costs of GenAI in Insurance

Before implementing a GenAI solution, insurers should conduct thorough cost-benefit analyses and long-term strategic planning so they understand the potential impact on their organization.

When looking at costs related to GenAI, there is a large spectrum. The costs for developing a simple proof of concept (PoC) or building something for personal use are very minimal. As bigger organizations, however, insurance carriers need to be aware of licensing.

Large insurers generally require more hardware for more users and increased data storage for larger data sets. Developing a simple PoC or small project for one or two users can be very simplistic, but if that PoC needs to be taken to production, the costs associated with the full solution must be weighed.

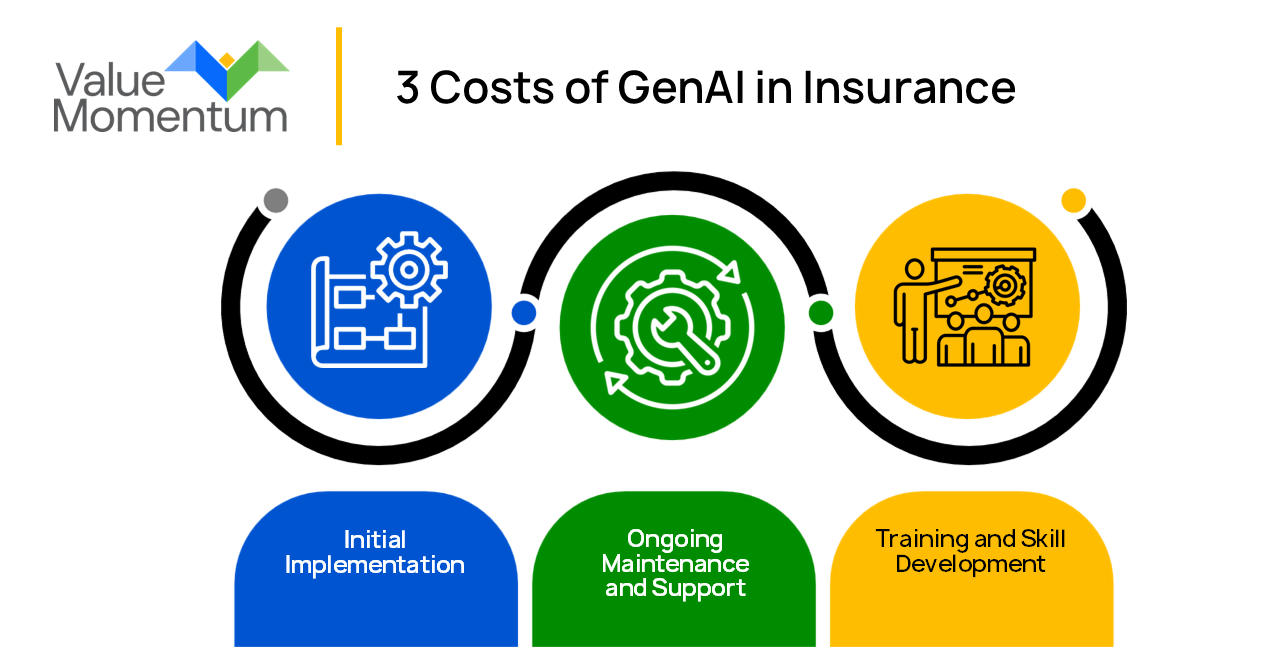

Here are three costs insurers should keep in mind during their cost-benefit analysis:

- Initial implementation The cost to implement a GenAI project can be significant, encompassing technology acquisition, integration, and training expenses. According to enterprise software development company Itrex, the cost of implementation can range from hundreds of dollars to up to $190,000 or more for a custom GenAI solution. These costs are critical, however, to ensure a tool is effective for its particular organization, and they include hardware, software, and data storage.

- Ongoing maintenance and support. Additionally, ongoing maintenance and support costs are essential to ensure that AI systems remain up to date, secure, and functioning optimally. This includes annual maintenance costs of the system itself as well as the cost of cloud computing to run the model, ongoing support from AI engineers and data scientists, and any future updates to the system and infrastructure. These ongoing costs can add up, ranging from $350k to $820k each year, according to ScaleupAlly. However, since these numbers are for full projects, they might be able to be shared with other project costs.

- Training and skill development. Ernst and Young (EY) found that almost half of insurers have no plans to train their workforce on AI. When used incorrectly, GenAI could generate the wrong information, damage an insurer’s relationship with its customers, and even learn the wrong information over time — remember, GenAI will continue to learn over time and adapt the more a company uses it. Investing in training and skill development ensures that carriers have the in-house talent to leverage AI capabilities strategically and derive maximum value from their investments. Developing a skilled workforce requires substantial investment in training programs, workshops, and certification courses.

There’s no question that insurers must understand the costs associated with adopting GenAI, but, when done strategically, these investments can yield both operational and financial benefits.

How to Assess GenAI’s Impact

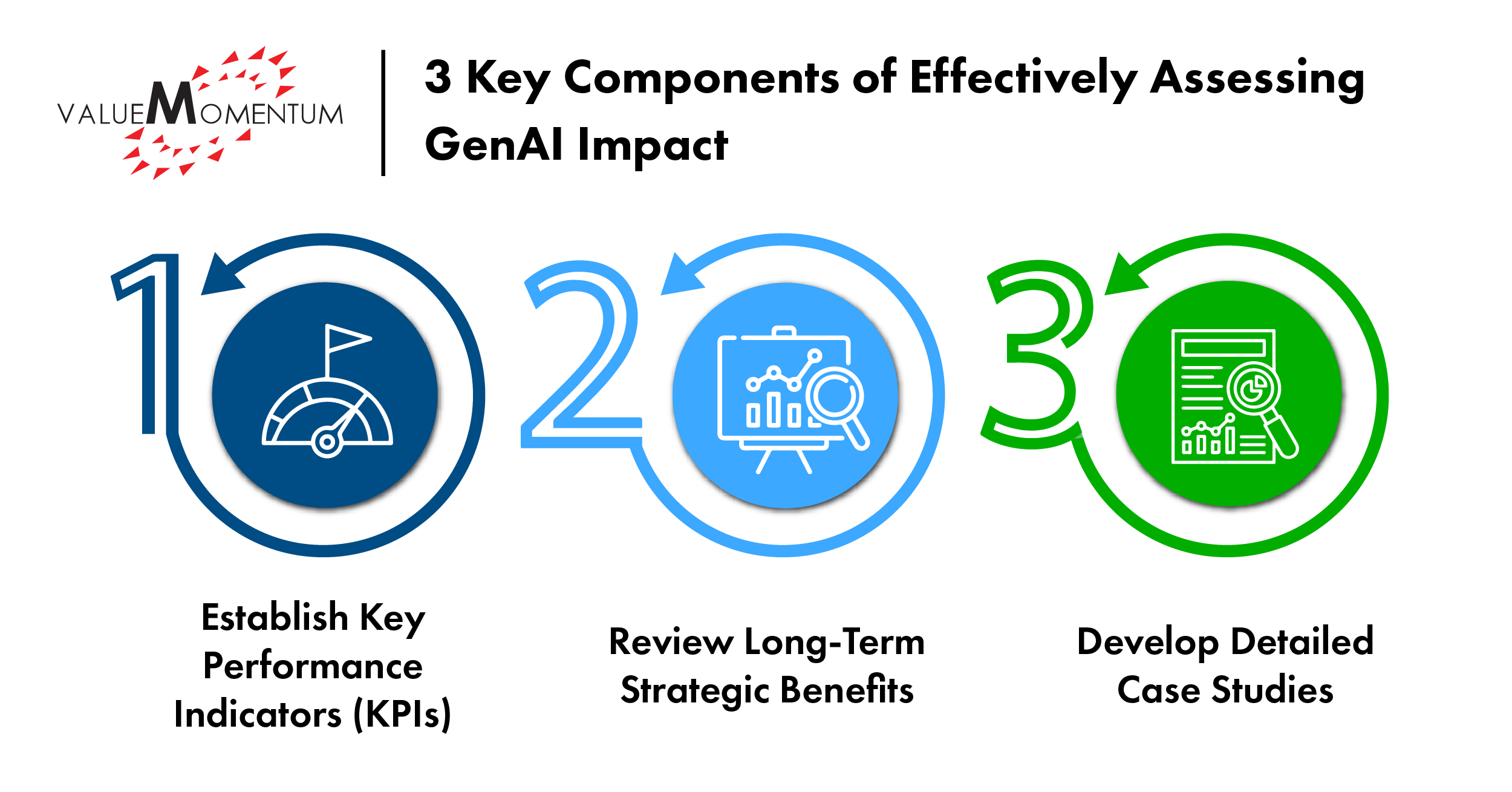

Once an insurer has conducted its cost-benefit analysis and decided to implement GenAI, the organization needs to measure GenAI’s effectiveness. Measuring the success of GenAI in insurance will help insurers make informed decisions about their investments and determine their next steps, including whether they want to expand their usage of the technology. Here are three key components of effectively assessing GenAI’s impact:

1. Establish Key Performance Indicators (KPIs)

Defining relevant KPIs is the cornerstone of measuring GenAI’s impact. These metrics should align with the insurer’s strategic objectives and provide quantifiable evidence of GenAI’s contributions. Examples of KPIs include:

- Reduction in policy generation time

- Improvement in customer satisfaction scores

- Increase in operational efficiency

- Cost savings achieved through automation

Regular monitoring of these KPIs enables insurers to track progress, identify areas of improvement, and ensure that the usage of GenAI is aligned with the organization’s overall business goals. One thing to note is that AI and humans both have failure rates. Best practice is to map out the process you are trying to automate — attempt to calculate how long humans take, how often they conduct the process, and what their failure rate is. Then look to beat any (or all) of those factors.

2. Review Long-Term Strategic Benefits

While KPIs provide short-term insights, reviewing GenAI’s impact on long-term strategic objectives offers a broader perspective. Most carriers look at improving combined ratios, increasing direct written premium (DWP), and increasing customer retention ratios. Insurers should also assess whether GenAI is contributing to:

- Enhanced customer experiences

- Reduction of calls managed by humans

- Underwriting straight-through processing

- Development of innovative products and services

- Increased market share and competitive advantage

- Employee satisfaction

None of these things can only be attributed to your GenAI journey. If you don’t already have an AI strategy with a subsection on GenAI that defines what these tools can do for you, stop now and create that. Each company is going to have a different focal point for how it wants AI to move the company. By evaluating GenAI’s impact on these strategic areas, insurers can make informed decisions about continued investment and resource allocation.

3. Develop Detailed Case Studies

PoCs and case studies are powerful tools for showcasing the tangible benefits of GenAI in insurance. They provide real-world examples of how insurers have successfully implemented GenAI, highlighting issues carriers faced, solutions implemented, and outcomes achieved. Case studies should include:

- The initial challenges faced

- Specific details about GenAI’s role in a project

- Quantifiable results and impact on the business

- Lessons learned and recommendations

Sharing these case studies with stakeholders fosters a culture of innovation, encourages knowledge sharing, and helps insurers benchmark their progress against industry peers.

By adopting these three approaches to measurement, insurers can comprehensively assess the impact of GenAI at their organization and make data-driven decisions to optimize their use of this technology. This ensures that GenAI continues to drive innovation, enhance customer experiences, and contribute to the long-term success of the carrier.

The Future of GenAI in Insurance

While the up-front investment required to support GenAI initiatives can be substantial, GenAI also has the potential to revolutionize the way insurers operate, from underwriting to claims processing to customer service. By leveraging its full potential, insurers can create more efficient and effective processes, reduce costs, and improve the customer experience.

By carefully measuring their return on investment and leveraging the strategic advantages of GenAI, insurers will be well positioned to succeed in the years to come.

To learn more about leveraging AI for better operational efficiency and improved business outcomes, read our case study, “Fortune 500 Insurer Revolutionizes Homeowners With AI and Aerial Imagery.”