For most P&C insurers, insurance pricing models and rating systems have long operated as back-office functions — important, but slow, opaque, and deeply entangled with legacy core systems. The consequences are familiar: rate changes that take months instead of days, actuarial teams spending more time on spreadsheet maintenance than model development, and limited visibility into how pricing decisions are actually affecting portfolio performance.

According to hyperexponential’s 2025 State of Pricing report, 85% of actuaries still rely on spreadsheets as a core part of their pricing stack. And nearly half cite lack of version control as a top barrier to maintaining and deploying pricing models. To fix this problem, insurers need to centralize their pricing logic rather than having it embedded across multiple core systems and miscellaneous spreadsheets.

When an insurance pricing engine platform operates as an independent function with its own data infrastructure, modeling environment, and deployment capabilities, actuaries can model, test, and deploy rate changes without waiting for IT. Insurance rate modeling stops being a bottleneck and starts being a competitive asset. But getting there requires more than a platform swap; it requires building, or rebuilding, an entire ecosystem of interconnected capabilities.

What’s Holding Insurers Back From Modern Pricing Models

Legacy pricing environments share a common set of structural failure modes that limit how effectively insurers can compete on price. Understanding them is the first step toward addressing them.

The most fundamental is the coupling of pricing logic to core policy administration systems. When rate changes require IT involvement — such as code deployments, release cycles, and regression testing — the business loses the ability to respond to market conditions at the speed those conditions demand. Pricing in insurance underwriting becomes reactive rather than strategic.

Fragmented pricing data compounds the problem. In most legacy environments, the data needed to build and deploy accurate insurance pricing models lives across multiple systems, including policy administration, claims, billing, and third-party data feeds, with no consistent, pricing-ready view. Actuaries spend significant time assembling and cleaning data before they can model anything, which limits both the frequency and quality of model updates.

Transparency and version control are typically casualties of this fragmentation. Without a structured audit trail of model changes, rate filings become slow, manual, and error-prone. Regulatory submissions require reconciling changes made across spreadsheets and systems, and the risk of filing errors grows with each update cycle.

Underlying all of these issues is an actuarial enablement gap. Even when data is available and systems are accessible, actuarial and product teams often lack the tools to independently test, simulate, and deploy pricing changes, leaving the function dependent on IT for execution and constrained in both pace and ambition.

These execution blockers point to the same conclusion: Modernizing insurance pricing models and rating systems is not an incremental improvement. It is a structural shift.

The Anatomy of a Modern Pricing Function

To stay competitive, insurers need to move beyond static rate models and periodic updates. This means investing in dynamic pricing capabilities that allow for continuous modeling, simulation, and refinement as risk conditions evolve, not just at annual review cycles.

It also means treating data as infrastructure: systematically integrating internal policy and claims data with third-party sources such as catastrophe models, telematics feeds, and economic indicators so that pricing decisions are grounded in the most current and complete available picture of risk.

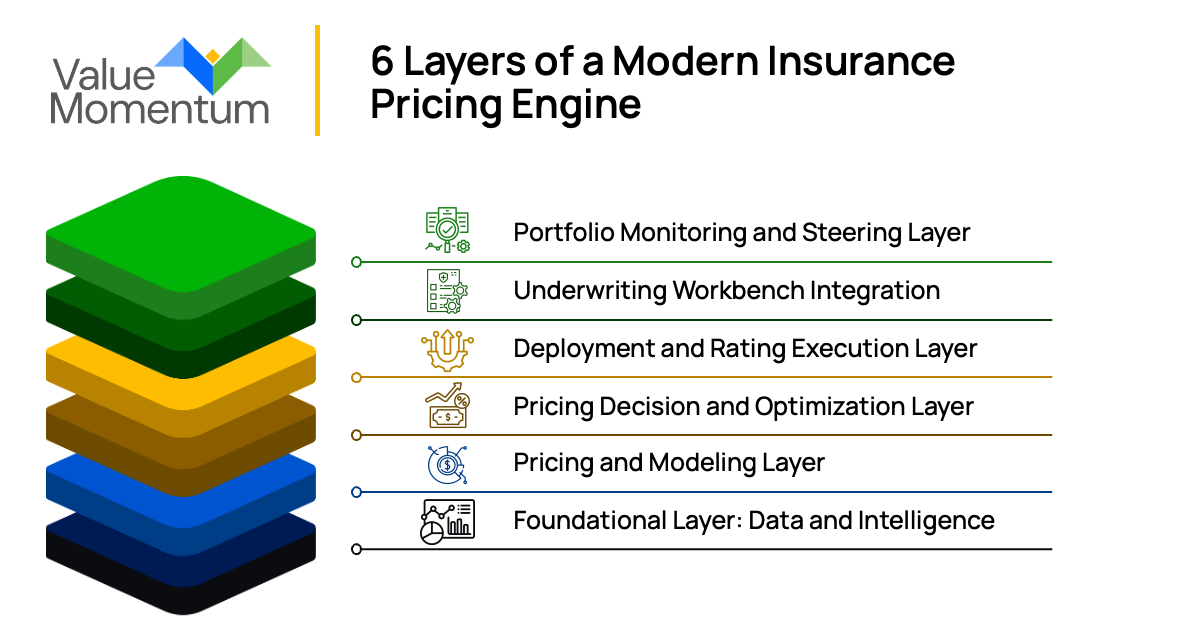

The following six-layer framework depicts what a modern insurance pricing engine platform looks like when these capabilities are fully realized.

Foundational Layer: Data and Intelligence

Every modern pricing function is built on a consistent, accessible, and pricing-ready data foundation. This means consolidating policy and claims data into a unified data lake structured at the exposure level; integrated with bureau content and standards-based templates (SBTs); and enriched by external sources such as catastrophe model inputs, economic indicators, telematics feeds, and industry benchmarks.

Real-time portfolio performance dashboards and data quality monitoring ensure that the information actuaries are working with is both current and trustworthy. Without this foundation, everything built on top of it is compromised.

Pricing and Modeling Layer

With a reliable data foundation in place, actuaries can build and maintain the models that drive pricing decisions. Modern insurance pricing models move beyond traditional generalized linear models (GLMs) toward machine learning approaches that support deeper segmentation and more complex risk relationships. Scenario modeling allows actuaries to simulate portfolio impact before deployment, replacing the guesswork of legacy cycles with pre-deployment visibility.

A rate adequacy engine tracks whether current rates are keeping pace with loss experience, while indication tracking and version control create an auditable record of model changes over time. Expense, reinsurance, and capital load integration ensure pricing decisions reflect the full cost structure of the business.

Platforms such as Earnix, hyperexponential, and Guidewire PricingCenter provide purpose-built actuarial modeling environments that operate independently of core policy systems, enabling the actuarial independence that legacy architectures make impossible.

Pricing Decision and Optimization Layer

Accurate loss models are necessary but not sufficient for competitive pricing. Insurers also need to understand how pricing decisions affect customer behavior — who buys, who stays, and who leaves. Win probability models estimate the likelihood of binding a quote at a given price point, allowing pricing teams to calibrate competitiveness by segment.

Retention models do the same for renewal pricing, identifying where rate increases are likely to drive lapse and where there is room to hold. These feed a discount guidance engine and a target price recommendation engine that give underwriters structured guidance at the point of decision — replacing ad hoc judgment with analytically grounded guardrails. Segmented pricing strategies ensure that pricing is tailored to the risk and demand characteristics of each segment rather than applied uniformly across the book.

Deployment and Rating Execution Layer

A pricing model that cannot be deployed quickly has limited competitive value. The centerpiece of this layer is a decoupled rating engine — a system that executes pricing logic independently of the core policy administration system via API-based pricing calls. This decoupling is what makes rapid, low-risk rate changes possible. Product configuration is managed through a separate layer that allows business users to adjust rules and parameters without development work, and microservices-based deployment ensures changes can be pushed incrementally rather than as monolithic releases.

Continuous deployment capability means rate changes are no longer batched into quarterly or annual cycles. Rate testing and regression validation are built into the process, ensuring every deployment is verified before it reaches the point of sale.

Underwriting Workbench Integration

A pricing function that operates in isolation from underwriting is only partially effective. This layer closes that gap by surfacing pricing intelligence directly in the underwriter’s workflow at the moment decisions are being made. Real-time price guidance gives underwriters visibility into the analytically derived target price for a risk, alongside the risk score that informed it. Referral triggers flag submissions that fall outside defined parameters, and authority controls define the boundaries within which underwriters can exercise discretion.

Override tracking creates an auditable record of every deviation from model recommendations and, over time, patterns in that data reveal where models may be miscalibrated or where additional guidance is needed. Done well, this layer ensures that the sophistication built into the pricing models above actually influences the prices that go to market.

Portfolio Monitoring and Steering Layer

Pricing doesn’t end at deployment. The portfolio monitoring and steering layer closes the feedback loop by tracking how pricing decisions are actually performing in the market and in the book.

Segment loss ratio dashboards and hit ratio tracking by tier give pricing teams a clear view of where the portfolio is performing as expected and where it isn’t. New versus renewal quality monitoring tracks whether the business being written today will be profitable tomorrow. Drift detection alerts flag segments where actual performance is diverging from pricing assumptions — creating an early warning system that allows actuaries to intervene before adverse trends become adverse results. Appetite and segmentation management tools round out the layer, giving leadership the visibility needed to steer the portfolio toward target segments and away from underperforming ones.

While these six layers are critical, a modern pricing architecture does not become effective simply by implementing new platforms. It requires a deliberate transition of actuarial workflows, governance, and operating models so that the capabilities described above are fully operationalized.

Actuarial teams must move from spreadsheet-centric model development toward platform-based insurance rate modeling environments where models, assumptions, and pricing logic are version-controlled, testable, and deployable. This transition typically involves migrating legacy pricing models, establishing standardized modeling workflows, and enabling actuaries to independently simulate and deploy rate changes without relying on IT release cycles.

Equally important is governance. Model versioning, rate indication tracking, scenario testing, and regulatory documentation must be embedded directly into the pricing platform so that actuarial teams can maintain a clear audit trail from model assumptions to deployed rates. This allows pricing decisions to be transparent, explainable, and aligned with regulatory expectations.

Finally, organizations must invest in enablement. Training actuarial and product teams to operate within modern insurance pricing engine platforms ensures that the full pricing stack — from data infrastructure to portfolio monitoring — is used effectively. When this transition is done well, actuaries spend less time maintaining models and more time analyzing risk, improving segmentation, and steering portfolio profitability.

From Back Office to Growth Engine

Modernizing insurance pricing models and rating systems is not a single project with a defined end state; it is an ongoing capability build. Carriers that invest in the full stack, from data infrastructure through portfolio monitoring, gain something their competitors on legacy architectures cannot easily replicate: the ability to price accurately, deploy quickly, and learn continuously from every quote and policy in the book.

As the P&C market continues to demand faster, more precise pricing decisions, the gap between carriers operating modern insurance pricing engine platforms and those still dependent on spreadsheets and coupled core systems will only widen. Carriers that begin building now will widen that gap in their favor.

Want to know more about how to evolve your pricing and underwriting with today’s technology? Watch our on-demand webinar, “AI Insider Insights: How Leading Insurers Are Transforming Underwriting with AI.”