Climate change is not just an environmental crisis — it’s a social and economic one that disproportionately affects vulnerable populations. Natural disasters like hurricanes, wildfires and floods wreak havoc year after year, with properties often rebuilt to inferior construction standards. Meanwhile, unchecked development exacerbates the problem, increasing runoff, erosion, and flooding. These compounding issues weaken communities’ resilience to the growing threats of climate change.

Equity is also at stake. Hurricane Katrina stands as a stark reminder of how marginalized communities bear the brunt of climate disasters. In New Orleans, the Lower Ninth Ward — a predominantly Black, low-income neighborhood — was among the hardest hit when the levees failed. Nearly two decades later, these disparities continue to persist, revealing systemic gaps in disaster preparedness and recovery efforts that must be addressed.

As climate risks escalate, the insurance industry is uniquely positioned to drive meaningful change. We may not yet know the cost of the vast damage caused by this past year’s hurricane season or understand the full scope of the destruction caused by the ongoing fires in Los Angeles, but we do know that insurers, customers, and communities need to make changes. Natural disasters in 2024 cost around $182.7B, just shy of double 2023’s $92.9B.

While economic losses are always higher than insured losses, climate resiliency practices can help fortify individual properties and communities against the increasing onslaught of natural catastrophes. Insurers like Travelers are already investing in strategies to help strengthen the communities they serve, such as coastal communities.

Climate Change and Insurance: A Stormy Relationship

Insurance thrives on data, and history shows how access to reliable information can drive transformative safety standards. Take seatbelts, for example: As insurers collected and analyzed accident data, they championed the adoption of safety belts, leading to significant reductions in fatalities. Similarly, workplace safety initiatives, informed by data on common hazards, have made industries safer and reduced claims over time.

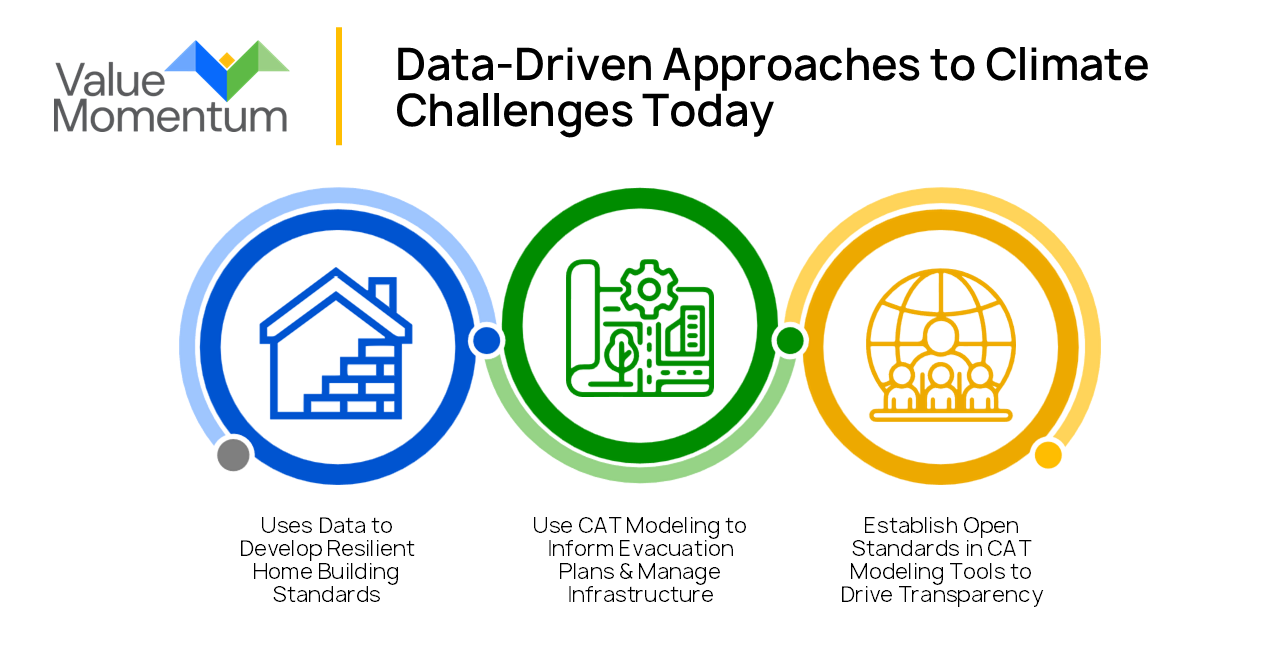

Today, those same principles are being applied to climate challenges. Organizations like the Insurance Institute for Business & Home Safety (IBHS) are using data to develop and advocate for resilient home building standards, helping communities withstand severe weather events. Beyond individual properties, insurers are also contributing to city-wide resilience, using catastrophe models to inform evacuation plans and manage critical infrastructure in the face of growing climate risks. Other organizations like The Institutes’ Catastrophe Resiliency Council are working to establish open standards through catastrophe modeling tools to help more players coexist in the ecosystem of modeling such events and drive greater transparency for all stakeholders.

Despite these efforts, much more needs to be done — and quickly. As climate change fuels more extreme weather events, new risks are emerging, such as the heightened potential for oil spills caused by monster storms disrupting infrastructure. Some regions in the U.S. are even becoming uninsurable due to escalating costs and risks.

Addressing these challenges requires urgent, coordinated action to protect communities, manage evolving threats, and ensure insurance remains accessible. Luckily, :

- Micro-Insurance: Provides direct coverage to individuals or small businesses, offering a safety net for those most vulnerable to climate impacts. While its adoption is growing in developing countries, its reach remains modest compared to its potential.

- Meso-Insurance: Covers groups or collectives, such as farmer organizations, where payouts are made to the group and distributed to members. This model allows for targeted support while spreading risk across multiple beneficiaries.

- Macro-Insurance: Designed for public or large private entities, this coverage funds large-scale recovery and reconstruction efforts. By insuring against catastrophic events, macro-insurance supports rebuilding entire communities and critical infrastructure.

However, while these diverse insurance models highlight how the industry is adapting to the escalating challenges of climate change, there are other hurdles to overcome, such as politics and bias.

Political resistance has created roadblocks, as seen in the April 2024 relaunch of an insurers’ climate alliance following a wave of member withdrawals. At the same time, the growing reliance on AI to manage climate-related risks brings its own complications. Concerns over bias in AI models, such as those highlighted in the “Model Bulletin on the Use of Artificial Intelligence Systems by Insurers,” underscore the need for transparency and careful oversight. Addressing these issues is critical to ensuring that insurance solutions remain equitable and effective in the face of escalating climate risks.

If insurers can successfully navigate these challenges, they can help their policyholders of all sizes recover from their losses, even in the face of disaster.

Adapting Insurance for Climate Resilience

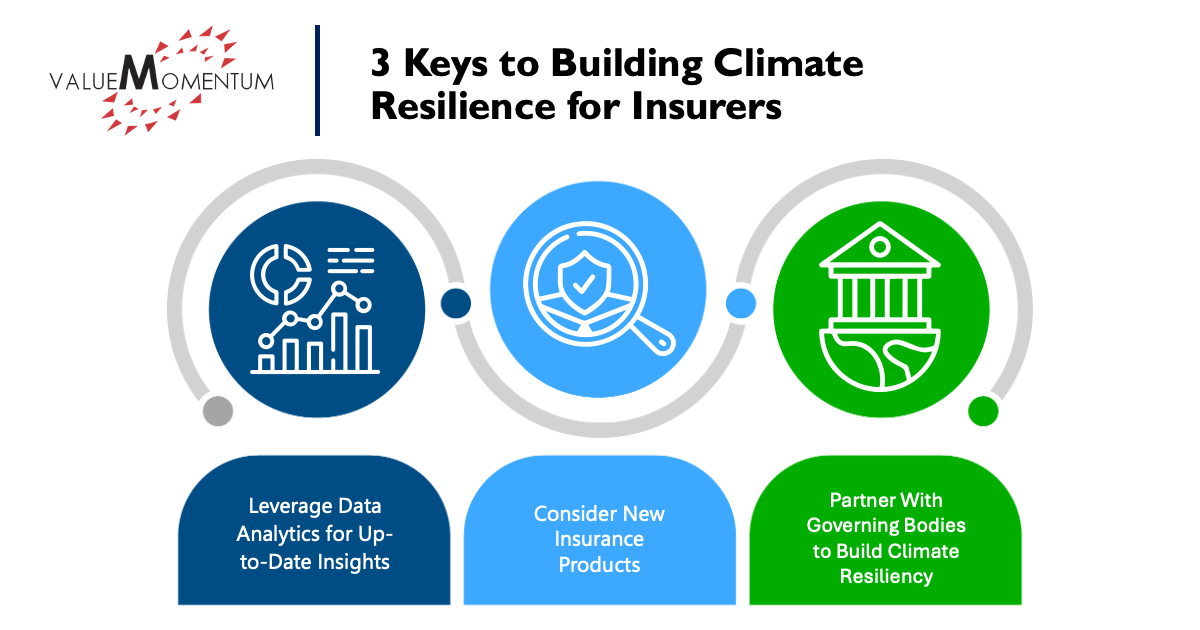

The growing frequency and severity of natural disasters demand proactive solutions that go beyond traditional practices. By harnessing the power of data and fostering innovation, insurers can not only address these challenges but also lead the way in building climate resilience. Here are three key takeaways for how insurers can adapt:

1. Leverage Data Analytics for Up-to-Date Insights

Savvy insurers are combining climate data with asset data to assess risks at an individual property level. By comparing factors such as a structure’s age, building materials, and location against storm damage models, or analyzing a farm’s water usage against heat and drought projections, insurers gain a more precise understanding of risk. Spatial analytics tools enhance this capability by enabling insurers to map flood zones, predict wildfire paths, and evaluate climate impacts with greater precision. Similarly, platforms that integrate environmental data, such as air quality and weather patterns, provide actionable insights to tailor coverage and manage risk effectively.

This detailed data translates into improved customer experiences. Hyperlocal analysis enables insurers to produce individualized risk scores, informing tailored coverage and pricing for businesses and properties. It also enhances transparency, empowering customers with the information they need to mitigate risks, which can reduce claims and potentially lower premiums.

Lastly, tools like Geographic Information System (GIS) software allow insurers to track incidents in near real time, helping them anticipate specific risks and accelerate claims responses after disasters, which is exactly what Travelers Insurance did to track hurricanes and wildfires, allowing the company to resolve 94% of claims within 30 days back in 2018. By leveraging these advanced data and analytics tools, insurers can improve their risk models, better serve their customers, and foster resilience in the face of escalating climate challenges.

2. Consider New Insurance Products

As climate risks intensify, the insurance industry must innovate to provide products that address emerging needs. For example, a collaboration between PartnerRe Ltd. and Farmers Edge leverages precision farming technology, such as satellite imagery and predictive modeling, to create tailored insurance solutions for farmers. These innovations help farmers mitigate risks while improving sustainability and efficiency, offering a model for how insurers can develop sector-specific products to meet the demands of a changing climate.

Parametric insurance is another promising avenue, offering faster payouts based on predefined triggers like weather conditions, rather than requiring lengthy claims processes. For instance, Arbol Inc.’s parametric reinsurance solution provided a $10 million payout to Centauri Insurance just three weeks after Hurricane Ian, using parameters such as the storm’s track and wind speed to determine the payment. Such products are particularly valuable in agriculture and other sectors where rapid financial relief can make the difference between recovery and collapse after extreme weather events.

Expanding these offerings can help insurers close coverage gaps while aligning with broader climate resilience goals. By combining advanced technologies with innovative policy design, the insurance industry can adapt to meet evolving challenges and opportunities.

3. Partner With Governing Bodies to Build Climate Resiliency

Collaboration between insurers and governing bodies is essential to close coverage gaps and improve climate resilience. The National Association of Insurance Commissioners (NAIC) recently adopted its first-ever National Climate Resilience Strategy for Insurance, focused on reducing losses and accelerating recovery from natural disasters. This strategy provides state insurance regulators with tools and an action plan to strengthen community resilience, including advocating for home hardening against wildfires, floods, and storms; utilizing catastrophe modeling; and improving public awareness of risks.

Additionally, the Partnership for Carbon Accounting Financials (PCAF) launched the Global GHG Accounting and Reporting Standard for Insurance-Associated Emissions, enabling insurers and reinsurers to measure and disclose greenhouse gas emissions tied to their underwriting portfolios. This standardized methodology offers deeper insights into portfolio risk profiles, fosters innovative decarbonization strategies, and ensures transparency for stakeholders.

By aligning with initiatives like the NAIC strategy and adopting global standards like PCAF’s methodology, insurers can drive meaningful progress in climate risk management while supporting resilience and sustainability goals at a systemic level. These partnerships underscore the critical role insurers play in fostering climate resilience and addressing the challenges of a rapidly changing environment.

Build Climate Resilience for a Stronger Future

While policyholders and insurers can’t prevent extreme weather events or natural disasters, they can work together to prepare more effectively and recover quickly when catastrophes do occur. Insurers can also collaborate with governing bodies to enact climate resiliency strategies and improve equitable outcomes for areas impacted by disasters.

Insurers are uniquely positioned to lead the charge against the growing challenges of climate change. By evaluating their underwriting portfolios to identify the highest exposures, supplementing traditional products with innovative options like parametric insurance, and partnering with stakeholders to strengthen building codes and resilience initiatives, they can help protect communities and ensure the availability of coverage.

To better prepare for and respond to climate-related risks, contact us to learn more about our Catastrophe Modeling and Exposure Management Services, which provide actionable insights to optimize underwriting decisions, manage portfolio exposures, and enhance overall resilience to climate change.