At 3°C of warming, capitalism will no longer be viable.

This was the stark warning from Günther Thallinger, board member at global insurer Allianz, signalling the scale of risk facing the insurance sector and wider economy as the climate crisis accelerates. At that level of warming, the impacts of extreme weather, resource scarcity and social disruption would be so severe that large parts of the world could become uninsurable, undermining the financial systems, markets and investment flows that capitalism depends on.

Although the worst impacts lie ahead, the effects are already unfolding in the UK, from flash floods in Yorkshire to rising threats along the Thames. One-third of critical infrastructure in England is now at risk of flooding, threatening the systems that communities rely on every day.

Insurers are central to building climate resilience. Beyond protecting assets, they have a powerful role in shaping policies, investments and practices that help communities adapt and thrive. This positions insurers as key drivers of systemic change.

The cost of failing to build climate resilience

As climate risks accelerate, financial and human costs are rising sharply. Around 6.3 million properties are already at risk from rivers, the sea or surface water, according to the Environment Agency’s National Flood Risk Assessment. This figure is expected to rise to one in four properties, or 8 million homes and businesses, by 2050. The financial cost is equally stark, with direct physical damage estimated at £2.4 billion a year and long-term economic losses reaching £6.1 billion annually.

These risks are already translating into higher insurance costs. UK insurers paid out a record £585 million for weather-related home and contents claims in 2024 alone, driven by 12 named storms, the highest number since 2015.

At the same time, climate change is forcing insurers, governments and communities to confront urgent questions about resilience and equity. A 2024 equity review by the UK Health Security Agency found that people in deprived areas face greater flood risks and are less likely to have insurance or protection. It also highlighted that flooding has a lasting impact on mental health, especially for those without insurance.

Insurers have the tools to lead

The insurance industry is uniquely placed to lead on climate resilience by connecting risk, finance and behaviour change. And this shift is already underway. Climate measures can protect not just individual properties but whole communities, and many UK insurers are investing in initiatives to support this wider goal.

For example, Aviva has committed over £80 million to nature-based solutions designed to reduce flood risks. The insurance provider was also among the first to join the Flood Re “Build Back Better” scheme, which offers up to £10,000 in extra funding for homeowners to install flood resilience measures during repairs after a flood.

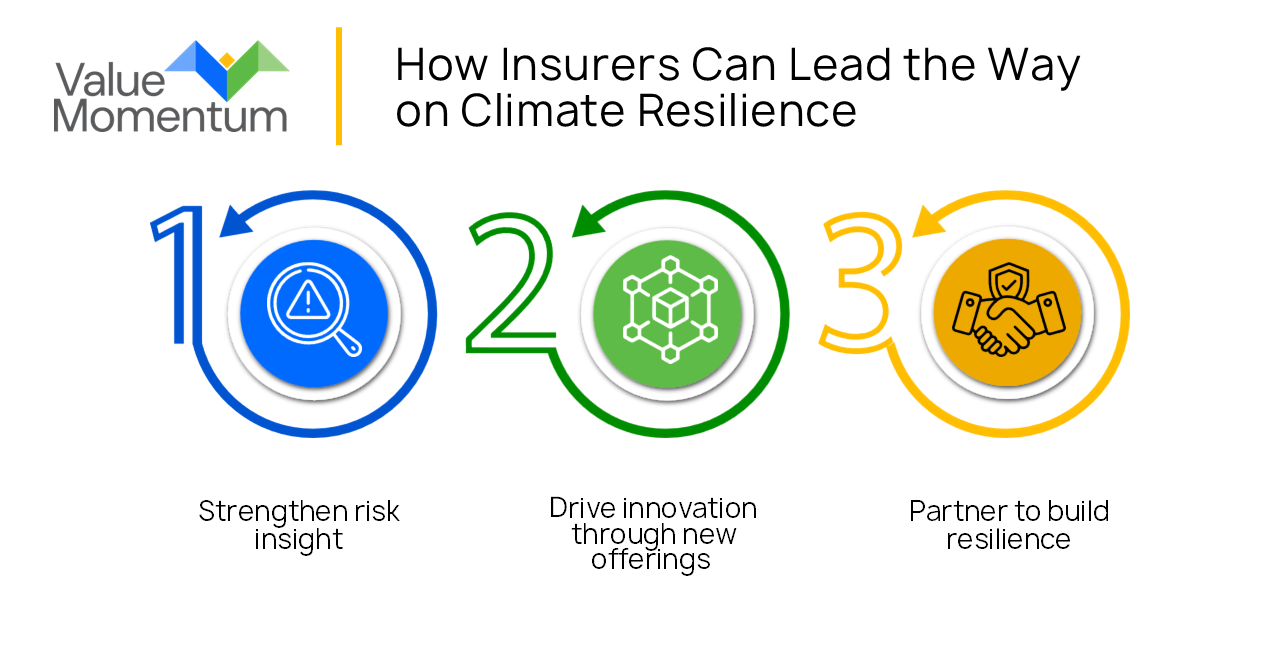

Investment alone is not enough. To tackle growing risks, insurers must combine data, innovation and collaboration. Here’s how they can lead the way.

1. Strengthen risk insight

Better data helps insurers make smarter decisions about underwriting, pricing and prevention. By combining climate and property data, insurers can assess risks at an individual level, from flood exposure to heat or fire risk. Spatial tools and environmental data platforms offer even more insight, helping insurers tailor coverage and support customers to manage their own risks.

For example, international insurer RSA uses Geographic Information System (GIS) technology to map flood zones, identify claims hotspots and improve disaster response. By integrating ArcGIS into its core systems, RSA enables underwriters and pricing teams to access real-time risk intelligence, enhancing decision-making and customer support.

Detailed data like this not only improves claims responses but also helps customers understand and reduce their own risks.

2. Drive innovation through new offerings

As climate risks change, insurance products need to keep pace. New approaches, such as parametric insurance, which provides payouts based on predefined triggers like rainfall levels or wind speeds rather than traditional loss assessments, offer faster support to people and businesses affected by extreme weather.

In the UK, FloodFlash’s parametric cover is helping small businesses in high-risk flood zones access insurance that is often unavailable through conventional products. Operating as a Lloyd’s coverholder with capacity support from Munich Re, FloodFlash speeds up recovery and helps close protection gaps for those who need it most.

By combining technologies like sensors, satellite data and predictive models with flexible and innovative product design, insurers can offer faster and more effective support to customers.

3. Partner to build resilience

Climate resilience cannot be delivered by insurers alone. It depends on collaboration across government, industry and local communities. The UK Government’s Flood Re scheme is one example of how partnership can make flood cover more affordable for households most at risk. It works by helping insurers offer lower premiums and excesses to eligible properties in flood-prone areas.

The Environment Agency’s Flood and Coastal Erosion Risk Management Strategy also calls for better use of data, stronger local partnerships and adaptive infrastructure to prepare communities for the future.

At the same time, accountability and emissions transparency are becoming central to building resilience. Frameworks such as the Green Finance Strategy and the Partnership for Carbon Accounting Financials give insurers tools to measure and disclose the emissions linked to insurance portfolios and investment decisions.

By working across sectors and engaging in these strategies, insurers can help reduce risk, support decarbonisation and strengthen long-term resilience.

Turning insight into action

The financial and social impacts of climate risk are rising, and insurers must play a critical role in shaping the response. This means not only offering products but sharing insight and strengthening prevention. For UK insurers, the stakes are high, but so is the opportunity to lead.

By embedding climate intelligence into risk assessment and underwriting, adopting effective catastrophe modelling and partnering with ecosystem and government organisations, insurers can both protect their portfolios and deliver long-term value to society. In the end, climate resilience will be judged by outcomes, not intentions.

Learn more about how ValueMomentum and our Risk Management services, including catastrophe modelling, analytics and insights, can help you build climate resilience into the fabric of your organisation.