Insurers do not set out to underpay customers. But most claims organisations are working with inherited methodology and out-of-date knowledge management solutions, which can fail to flag problems along the claims life cycle.

This technology lapse came to a forefront in March 2024, when the FCA published a multi-firm review that covered up to five years of claims outcomes across 12 insurers (roughly 90% of the market). The regulator documented a total redress reaching £200 million across 270,000 policyholders.

While the data existed throughout, and the pattern was visible, critical insights were not surfaced for human review early enough to prevent outdated workflows from leading to poor outcomes. Consumer Duty has now made addressing these types of issues a priority for UK claims organisations.

For chief claims officers, optimising claims knowledge management is a crucial practice to bring actionable insights to light earlier in their workflows. With AI-powered knowledge solutions, UK insurers can act on the signals already sitting within their claims data to provide fair payouts and avoid regulatory issues.

What analytics-driven knowledge solutions bring to the table

Better claims knowledge management does not require building a perfect data environment from scratch. Insurers have the information required. However, they need to make better use of what already exists, starting with the parts of the claims journey where earlier and more consistent decisions have the greatest impact on cost and customer outcomes.

First notice of loss (FNOL) is the most important intervention point. It is where the handling path is still open, where fraud and complexity signals are most actionable and where routing decisions shape everything that follows. Stronger triage at that stage, informed by comparable cases and clearer guidance, reduces leakage before it builds rather than after it has already become embedded.

Consider a household escape-of-water claim during a cold spell. If the system can recognise that similar cases with the same combination of property type, repair history and early severity indicators have consistently developed into high-cost claims, it can flag the file immediately for specialist review and earlier supplier engagement. Repeated across thousands of similar claims, the cumulative effect is significant.

The same principle applies to inconsistency of the kind the FCA identified in motor total loss. Where handlers are drawing on different information, applying different assumptions or working without visibility of how comparable cases were resolved, variation is inevitable.

Connecting the data, surfacing relevant precedent and making guidance accessible within the flow of work helps handlers cut through information overload, make faster and more confident decisions, and reduce that variation without removing the human judgement that remains essential. It also makes it easier to explain why a file was routed, escalated, settled or investigated in a particular way, which is increasingly important for internal oversight as well as external scrutiny.

The road to analytics-driven claims management

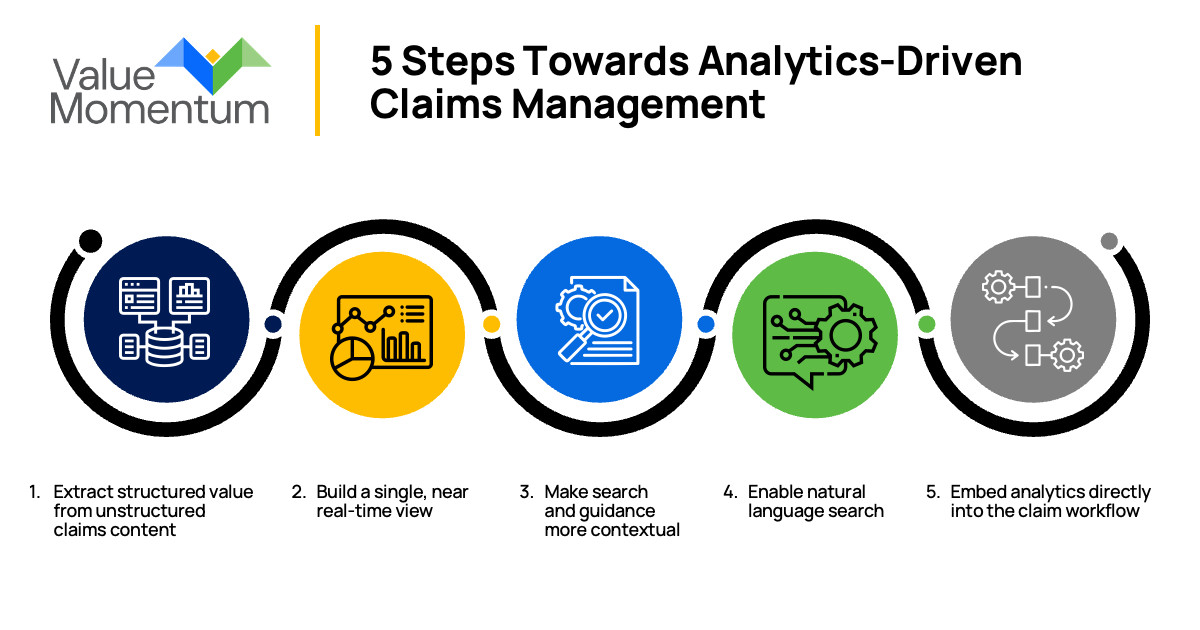

The firms making the most progress are focusing on a small number of practical capabilities rather than attempting a wholesale transformation. Here is where to start.

- Extract structured value from unstructured claims content. This includes notes, images, correspondence and reports. Turning unstructured data into structured data is the foundation of an analytics-driven knowledge solutions, because much of the context that shapes a claim still sits in formats that cannot be searched or compared at scale. That is one reason claims analytics has often underdelivered: too much of the signal sits outside clean, standardised fields and remains difficult to use consistently in day-to-day decision-making.

- Build a single, near real-time view. Connecting information from core systems and third-party inputs around each claim reduces the time handlers spend assembling information and increases the time they spend acting on it. In many insurers, however, claims data is still spread across core platforms, supplier systems and older repositories, which makes it harder to generate a complete picture early enough to support better decisions.

- Make search and guidance more contextual. Better context means handlers can find relevant policy wording, precedent and process guidance quickly, which improves both consistency and the ability to explain decisions clearly to customers and regulators. It also reduces reliance on individual experience alone, which is another common barrier to scaling analytics-driven decision support across the claims function.

- Enable natural language search. When handlers can search in natural language, it is easier to retrieve past claims knowledge and apply it at the point of decision. Having that information readily available from a simple search lets handlers compare a live claim with similar historical cases, surface relevant policy guidance and previous handling outcomes and receive prompts on the most appropriate next step based on the facts available at the time.

- Embed analytics directly into the claim workflow. When real-time knowledge support is embedded directly into the workflow instead of sitting in a separate tool, adoption is higher and the value is more immediate. Over time, the same environment should capture which actions were taken, what outcomes followed and where decisions later proved weak, so that firms can refine guidance, improve models and strengthen consistency across the claims book.

Across all of these steps, the principle is the same. Decision support should surface the right information early, provide relevant recommendations or next-best actions where appropriate and keep accountability firmly with the handler. The governance and auditability that Consumer Duty demands cannot be delegated to a model. They require human oversight, clear audit trails and leaders who understand what the system is doing and why.

The future of knowledge solutions for claims management

The total loss episode was a visible and costly example of what happens when patterns go unseen at scale, and it will not be the last. The FCA has already signalled that claims outcomes in household and travel remain under scrutiny, most notably in its review of home and travel claims handling arrangements and in subsequent supervisory action. The broader point is clear: Where firms rely on weak management information, fragmented oversight or customers failing to challenge poor decisions, the regulator has shown it is prepared to intervene.

For chief claims officers, the firms best placed to manage that scrutiny are not those with the most sophisticated models, but those with a clear view of what is happening across the claims book, the ability to explain their decisions and the operational discipline to act on what the data is showing before someone else identifies the issue for them.

To learn more about how insurers are reaping the benefits of advanced analytics and AI in their claims organisations, watch our on-demand webinar “Ask the Experts: Boosting Claims Efficiency & Effectiveness Through Intelligent Automation”.