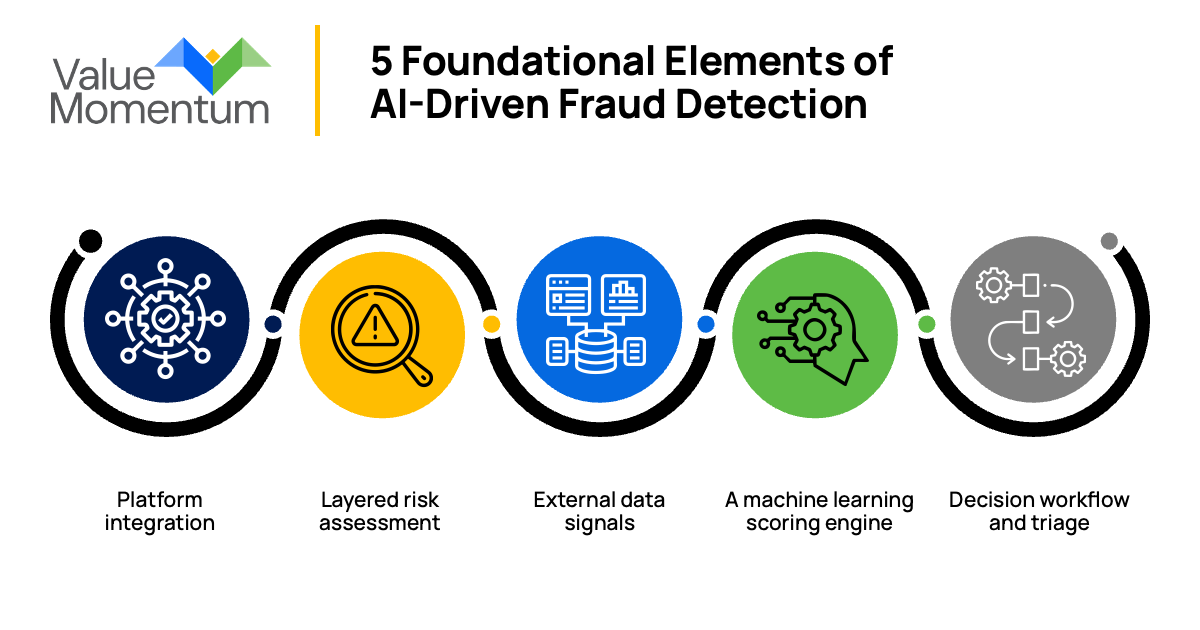

The foundational elements of AI-driven fraud detection

Effective fraud detection at scale requires an integrated framework connecting data, analytics and decision-making into a coherent operating model, embedded in the claims process from first contact.

Platform integration

Detection capability must also extend beyond core claims systems into first notice of loss (FNOL) platforms, telematics feeds, repair networks, digital submission channels and contact centre operations. Leading UK carriers are increasingly embedding fraud screening directly into operational workflows to ensure suspicious activity is identified before downstream costs such as credit hire, repair escalation or litigation exposure begin to accumulate.

Layered risk assessment

Modern UK fraud operations are also incorporating behavioural and voice analytics to detect inconsistencies, coached responses and emerging fraud patterns that static rules engines typically miss. This is becoming increasingly important as organised fraud networks adopt more sophisticated and AI-enabled approaches to claims manipulation.

External data signals

In the UK market, cross-ecosystem intelligence is becoming a major differentiator. Leading insurers are combining CUE data, geospatial analysis, solicitor and medical provider patterns, device fingerprinting and graph analytics to identify organised fraud rings operating across multiple claims and carriers simultaneously.

A machine learning scoring engine

Advanced fraud scoring engines increasingly provide real-time decision orchestration rather than simple risk alerts. The output can dynamically trigger SIU referrals, enhanced investigations, payment controls or straight-through processing depending on risk severity, helping carriers balance fraud prevention with customer experience and operational efficiency.

Decision workflow and triage

The most effective operating models include continuous SIU feedback loops, allowing investigation outcomes to retrain models and improve scoring precision over time. This helps reduce false positives, improves SIU productivity and enables fraud strategies to adapt more quickly as fraud typologies evolve.

As Consumer Duty and FCA scrutiny continue to increase, explainability and governance are becoming as important as detection accuracy itself. UK insurers are therefore placing greater emphasis on transparent AI models, auditable decision trails and human oversight controls to ensure fraud prevention frameworks remain operationally effective while supporting fair customer outcomes.

The strategic case for advanced fraud detection

Catch more fraud earlier and the benefits follow. Loss ratios improve, combined ratios tighten, SIU capacity goes where it is needed and legitimate claimants move through faster resulting in better claims experience and outcomes. The leading carriers have analytics built in from FNOL, detection that learns continuously and triage driven by data rather than individual handler judgement.