Claims is where policies are tested and customer trust is built or broken. For chief claims officers across property and casualty (P&C) insurance organisations, that pressure is intensifying. The 2026 Association of British Insurers (ABI) home and property claims report noted a record £6.1 billion in property claims paid out in 2025, driven by adverse weather, inflation and growing climate exposure.

Motor is under similar strain, with claims inflation in the high single digits and, at points, reaching double digits across repair, credit hire and personal injury lines, compressing margins and pushing severity higher. Fraud adds further pressure. In the UK, Aviva blocked over 6,000 fraudulent claims in the first half of 2025 alone, preventing more than £60 million in losses, a sign of the scale and sophistication of organised fraud activity across motor, property and liability.

Fraud adds further pressure. Per Aviva’s H1 2025 results announcement, the insurer blocked over 6,000 fraudulent claims in the first half of 2025 alone, preventing more than £60 million in losses, which is a sign of the scale and sophistication of organised fraud activity across motor, property and liability lines in the UK market.

At the same time, the FCA’s Consumer Duty framework requires firms to demonstrate, not merely assert, that claims outcomes are fair, with consistent, well-reasoned decisions from first notice of loss (FNOL) through to settlement. Following its December 2025 response to the Which? super-complaint, scrutiny of claims handling has sharpened further. Firms that cannot show the decision logic behind their outcomes face regulatory censure, potential remediation costs and reputational exposure.

Turning advanced analytics into a strategic advantage for claims

Despite the clear imperative, most insurers are still operating with models that are not equipped for this environment. Effective claims management requires analytics built for insurance, not generic models.

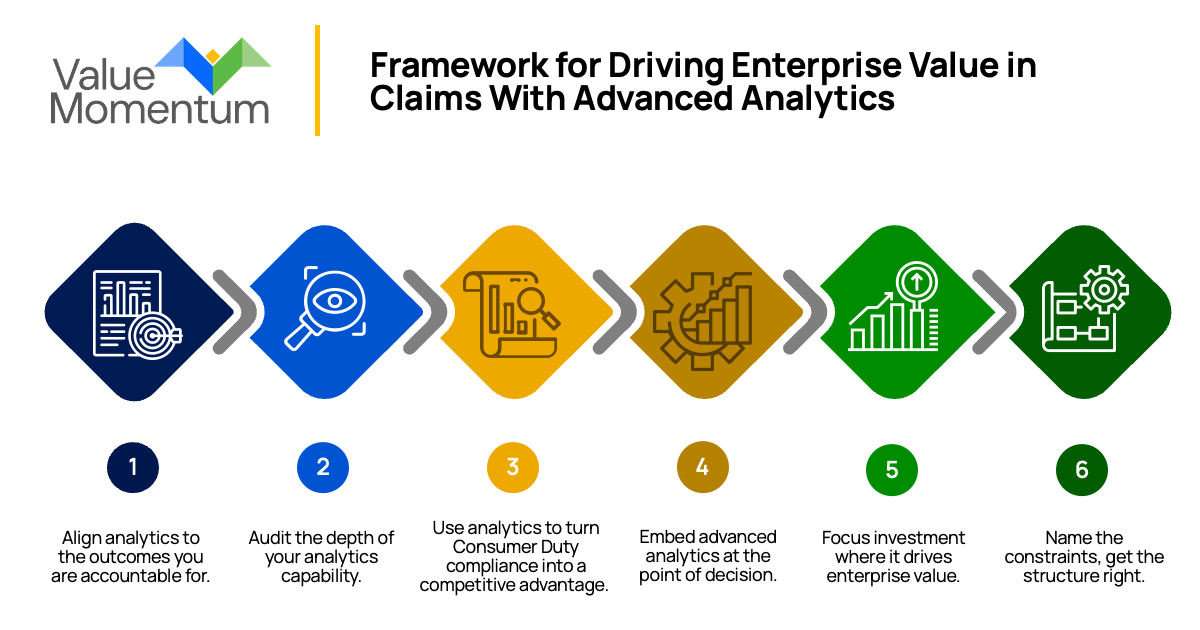

Here is a five-point framework for making advanced analytics a driver of enterprise value across the claims operating model.

1. Align analytics to the outcomes you are accountable for.

Every insurer needs a clear view of where advanced analytics can improve performance. Fraud detection, loss cost containment, customer satisfaction and subrogation recovery are all legitimate targets. The discipline is choosing which ones to prioritise and building the programme around them.

A regional Tier 1 P&C insurer with whom ValueMomentum has worked identified subrogation recovery as its most underleveraged opportunity and deployed a prediction model at FNOL, integrated directly into its claims platform.

Within 12 months it had achieved a 12% increase in subrogation recoveries, automated 25% of subrogation referrals through predictive models, and reduced average recovery cycle time from 154 to 124 days, across a portfolio of 59,500+ claims. The model worked because the business problem was clearly defined before the technology was chosen.

2. Audit the depth of your analytics capability.

Once strategic targets are set, the harder task is establishing where advanced analytics directly informs decisions and where it simply sits alongside them. Across the UK market, that spectrum is wide. At one end, data-aware organisations have dashboards, but decisions are still shaped by experience and precedent. Data-informed organisations use analytics to validate assumptions and support targets, but insight tends to arrive after the fact.

At the other end, a smaller group are genuinely data-driven. Predictive models shape FNOL routing, reserve logic and litigation flags, shifting the adjuster’s role from case-pusher to judgement-holder.

Most insurers remain some distance from that third category, and the gap matters. Consumer Duty requires firms to evidence fair outcomes at the level of individual decisions, not in aggregate. Following the FCA’s response to the Which? super-complaint, scrutiny has sharpened further, including how firms handle claims and oversee third parties.

3. Use analytics to turn Consumer Duty compliance into a competitive advantage.

A common concern among UK claims leaders is that analytics-driven decision-making may conflict with FCA Consumer Duty obligations. The opposite is true. Consumer Duty requires firms to evidence fair outcomes, and claims intelligence is precisely what makes that standard achievable in practice.

Analytics-driven settlement ranges create auditable evidence of fair value. Intelligent triage identifies vulnerable policyholders at FNOL and routes them appropriately. Generative AI produces plain-language explanations of decisions with a full audit trail. And claims data fed back into product design demonstrates the end-to-end accountability Consumer Duty was designed to drive.

Models designed for the UK market should include explainability outputs as standard, identifying not just what decision was made, but why and on what basis, through model-scoring logic and audit-ready decision logs. That is the difference between analytics that supports Consumer Duty and analytics that creates new regulatory exposure.

4. Embed advanced analytics at the point of decision.

Analytics accessed through a dashboard that adjusters check periodically is not the same as advanced analytics embedded in the workflow at the moment a decision is made. The distinction drives the outcome.

For most insurers, the starting point is early in the claims journey, where better input drives every downstream decision.

5. Focus investment where it drives enterprise value.

Advanced analytics delivers the most measurable returns in operational efficiency, FNOL decision-making and adjuster effectiveness.

Better visibility of expense and loss drivers, from loss ratios by line of business to recovery rates and attorney performance, allows claims teams to pinpoint where costs and inefficiencies sit. Process metrics such as cycle time, reassignments and path optimisation further improve how work flows through the function.

At FNOL, analytics strengthens decision-making by extracting insight from unstructured data, identifying claim severity from call transcripts and images and flagging indicators such as litigation risk, subrogation opportunity and loss estimates at first contact.

For adjusters, segmentation by complexity and automated assignment reduce cognitive load, while access to relevant past cases, coverage insights and performance data supports faster, more consistent decisions. In a UK market where specialist talent shortages are limiting operational capacity, using analytics to multiply adjuster effectiveness is a strategic workforce strategy, not just a technology investment.

6. Name the constraints, get the structure right.

Even sophisticated claims functions face the same constraints: siloed data, inconsistent quality and legacy systems that limit real-time access. Until that foundation is addressed, advanced analytics cannot deliver consistent value. The UK insurance market benefits from several shared industry data assets that strengthen claims analytics when properly integrated. Sources such as the Claims and Underwriting Exchange (CUE), the Motor Insurance Database (MID) and intelligence from the Insurance Fraud Bureau provide valuable signals on claims history, policy coverage and potential fraud activity.

When incorporated into claims analytics platforms, these data sources improve identity validation, uncover previously undisclosed claims and strengthen fraud detection models. For claims leaders, integrating these industry data sets alongside internal claims data can significantly enhance decision quality across the claims life cycle.

But how teams are structured determines whether analytics can scale. Centralised data science teams working in isolation produce outputs that front-line teams neither trust nor use. Leading insurers instead adopt a hybrid model: Enterprise teams manage infrastructure and governance, while embedded analytics sits within claims to shape solutions around real decisions. Some are formalising this through centres of excellence to drive consistency and scale.

Where advanced analytics earns its place

The insurers pulling ahead on loss ratio, fraud containment and customer outcomes share a common thread: analytics treated as a core operating discipline, not a peripheral capability.

Claims leaders assessing where analytics can most immediately impact their organisational practices should start with a structured diagnostic approach that maps current decision points against analytics maturity and quantify the leakage exposure at each stage. Having a clear view of where an enterprise’s economics are most exposed can help yield stronger return.

To learn more about how claims organisations are modernising with advanced technology, watch our on-demand webinar AI Insider Insights: AI Claims Use Cases.