Despite general insurers (GIs) understanding the need for pricing modernisation, many are still operating with legacy processes. Rate changes that should take days take months, spreadsheets still dominate actuarial workflows and there’s limited visibility into how pricing decisions impact portfolio performance. The problem isn’t the platform: It’s everything around it.

Historically, pricing logic has been coupled with core policy administration systems, which has meant that every component of a rate change was dependent on IT, limiting the business’s agility to respond to market shifts. This is exacerbated by information scattered across numerous systems and third-party data platforms, with no pricing-ready view of the data. Not only do these manual processes require actuaries to devote time to gathering and cleansing data prior to modeling, but they also intensify the possibility of manual errors and regulatory risk.

Even at insurance organisations with available and accessible data, many actuarial and product teams do not have the talent or tools to simulate or deploy pricing changes without IT. The Institute and Faculty of Actuaries (IFoA) has highlighted the shortage of actuaries with the data science skills needed to work across modern systems. This shortage is fuelling the growing number of pricing teams caught between maintaining legacy models and wanting to modernise their approaches.

The elements of a modern pricing function

Driving a competitive edge with pricing requires insurers to invest in modern approaches that enable continuous modelling and refinement alongside evolving risks, not reliance on static models that are updated on an annual review cycle.

It also requires rethinking the enterprise approach to data and viewing it as a foundational element of modernisation efforts. Internal data from policy and claims systems should be systemically integrated with third-party data feeds. This includes catastrophe models, telematics feeds and economic indicators to ensure that pricing decisions are grounded in a comprehensive understanding of risk. In the UK market, for example, the Environmental Agency estimates that around one in six properties are at risk of flooding. Dynamic, model-driven pricing of climate-related claims is becoming a necessity rather than an optional extra.

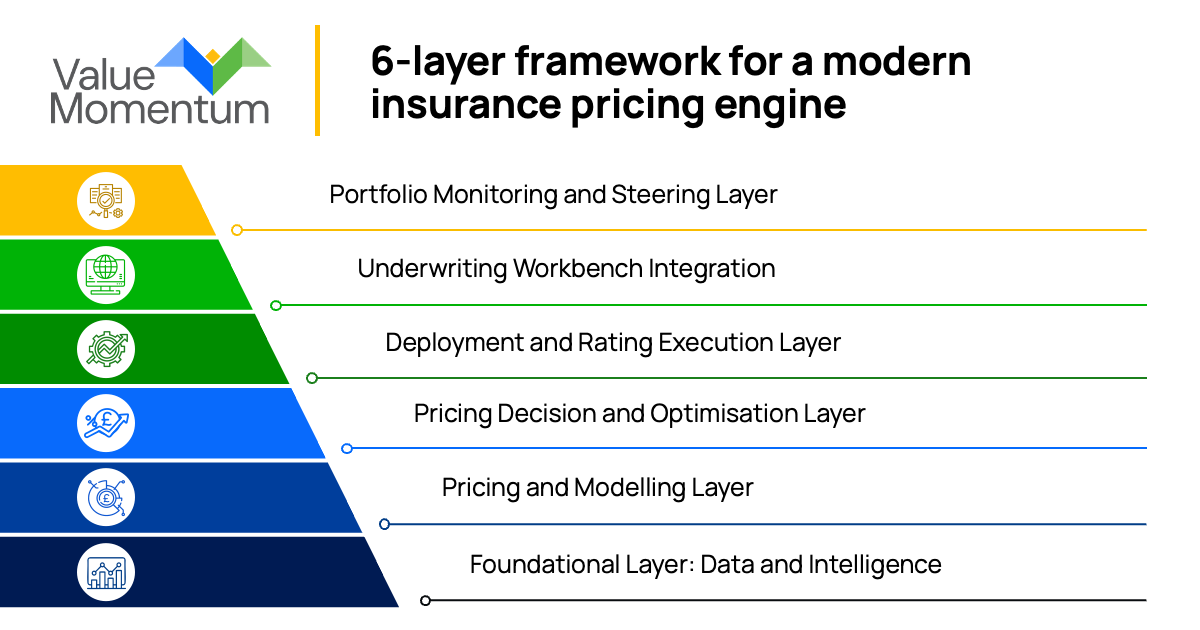

The following six-layer framework depicts what a modern insurance pricing engine platform looks like when these capabilities are fully realised.

Foundational Layer: Data and Intelligence

A modern pricing function depends on a pricing-ready data foundation where policy, claims, exposure and third-party data are continuously integrated, governed and enriched to support decision-making. Leading insurers are increasingly establishing pricing-specific data products that standardise and operationalise actuarial, underwriting and portfolio data for consumption across pricing workflows.

Without real-time portfolio performance dashboards and robust data quality monitoring, actuaries are working with incomplete data that skews their context and embeds those flaws into every subsequent layer built on top of this weakened foundation.

Pricing and Modelling Layer

With a solid data foundation, actuaries are empowered to develop and maintain the models that drive pricing decisions.While traditional approaches rely on generalised linear models (GLMs), modern pricing models utilise machine learning that supports deeper segmentation and more complex risk relationships. Scenario modelling replaces the guesswork of legacy cycles with pre-deployment visibility to simulate portfolio impact before deployment.

A rate adequacy engine ensures current rates remain aligned with loss experience, while indication tracking and version control maintain a full auditable record of model changes. Expense, reinsurance and capital load integration ensure pricing decisions reflect the full cost structure of the business.

Purpose-built actuarial modelling platforms such as Earnix, hyperexponential (hx), Guidewire PricingCenter and Radar (WTW) operate independently of core policy systems, giving actuarial teams the freedom that legacy architectures denied them.

Pricing Decision and Optimisation Layer

To price competitively, insurers must also understand the behavioural dimension, i.e. how pricing decisions influence who converts, who renews and who leaves. Win probability models give pricing teams the ability to estimate the likelihood of binding a quote at a given price point, enabling more precise calibration of competitiveness by segment.

The same logic applies to renewals. Retention models identify where rate increases risk driving lapse and where there is room to sustain — feeding into both a discount guidance engine and a target price recommendation engine that replaces underwriter instinct with analytically grounded decision-making.

This results in a segmented pricing strategy that reflects the true risk and demand characteristics of each segment rather than being applied uniformly across the book.

Deployment and Rating Execution Layer

Pricing models only create value when they can be deployed quickly. A decoupled rating engine, executing pricing logic independently of the core policy administration system via API-based pricing calls, is what makes it possible.

By separating product configuration into its own layer, business users can adjust rules and parameters without requiring IT involvement. Microservices-based deployment ensures changes can be pushed incrementally rather than as monolithic releases.

Continuous deployment capability means rate testing and regression validation are built into the process, ending the days of batching rate changes quarterly or annually.

Underwriting Workbench Integration

Pricing intelligence that never reaches the underwriter is a wasted source. This layer embeds pricing guidance directly into the underwriter’s workflow at the moment decisions are being made.

Real-time price guidance gives underwriters visibility into the analytically derived target price for a risk, alongside the risk score that informed it. Referral triggers flag submissions that fall outside defined parameters, while authority controls set clear boundaries within which underwriters can exercise discretion.

Every deviation from the model is captured through override tracking, creating an auditable record that, over time, will reveal where models need recalibration or where underwriters need additional guidance. It’s this layer that ensures the sophistication of pricing models actually translates into the prices that go to market.

Portfolio Monitoring and Steering Layer

Deployment is not the end point. The portfolio monitoring and steering layer exists to close the feedback loop, continuously tracking how pricing decisions are performing — both in the market and in the book.

Segment loss ratio dashboards and hit ratio tracking by tier give pricing teams a granular view of where performance aligns with expectations and where it doesn’t. New versus renewal quality monitoring keeps an eye on whether the business being written today will be profitable tomorrow.

Where actual performance begins to diverge from pricing assumptions, drift detection alerts provide actuaries with early warning, creating the opportunity to course-correct before adverse trends embed themselves in results. Appetite and segmentation management tools complete the layer, giving leadership the visibility to actively steer the portfolio toward target segments and away from those that are underperforming.

Extracting full value from a modern pricing architecture demands a deliberate transition of actuarial workflows, governance and operating models, not just a technology upgrade. Migrating legacy models and establishing standardised workflows are typically the starting point; the end goal is to empower actuarial teams to independently simulate and deploy rate changes.

Governance must be built into the platform itself, rather than bolted on afterwards. Model versioning, rate indication tracking, scenario testing and regulatory documentation embedded directly into the pricing environment give actuarial teams a clear audit trail from model assumptions to deployed rates.

This allows pricing decisions to be transparent, explainable and aligned with regulatory expectations, such as FCA Consumer Duty’s fair value requirements and Lloyd’s Project RIO. Continuously evolving regulation is only increasing the need for robust pricing governance, transparency and evidence‑based underwriting discipline.

From Back Office to Growth Engine

Insurers that commit to the full stack behind pricing modernisation, from data infrastructure to portfolio monitoring, gain something their competitors on legacy architectures cannot easily replicate: the ability to price accurately, deploy at speed and learn continuously from every quote and policy in the book.

As the GI market continues to demand faster, more precise pricing decisions, the gap between insurers who are truly operationalising their pricing capability and those still dependent on spreadsheets and legacy workflows will only widen.

Want to know more about how to evolve your pricing and underwriting with today’s technology? Watch our on-demand webinar, “AI Insider Insights: How Leading Insurers Are Transforming Underwriting with AI.”