Claims complexity is increasing, and so is the expectation that insurers make better, faster and more consistent decisions. In the UK market, claims is a board-level priority, with pressure on leaders to balance customer outcomes, fraud risk, cost discipline and regulatory scrutiny. Under the Financial Conduct Authority (FCA) Consumer Duty, firms must evidence that decisions are fair and well-founded, not simply efficient.

Despite sustained investment, many insurers continue to face structural operational challenges: fragmented data, manual workflows and limited decision visibility at critical points in the claims life cycle. These inefficiencies are amplified by acute talent shortages, particularly in specialist claims roles. Gallagher Bassett’s 2026 Claims Insights survey found more than 70% of UK insurers report difficulty securing specialist claims talent, with shortages now directly limiting operational capacity.

The combination of these pressures is most evident in claims leakage, where inefficiencies, inconsistent decision-making and process gaps drive a wedge between expected and actual claim costs. UK P&C carriers have historically experienced leakage rates consistent with the 5–8% industry average; litigated liability books frequently exceed this threshold. Yet most insurers lack the real-time measurement and diagnostic capability to isolate and address these drivers proactively.

By embedding advanced analytics, automation and decision support directly into the claims workflow, insurers can augment limited talent, standardise decision-making and actively prevent leakage rather than detect it after the fact.

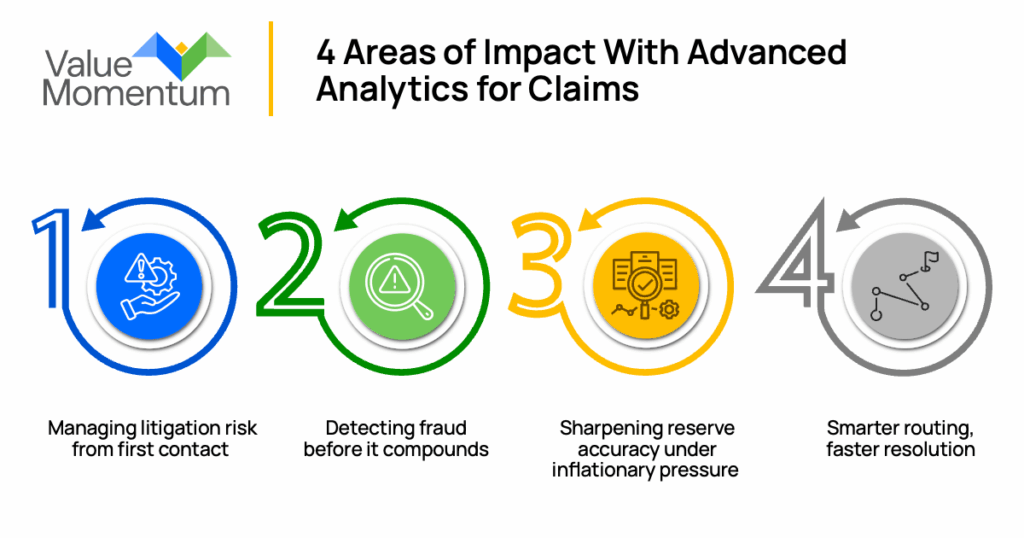

Creating impact with advanced analytics for claims

While analytics can influence every stage of the claims life cycle — from first notice of loss (FNOL) triage, severity prediction and coverage validation to recovery, experience monitoring and supplier management — the most immediate and visible impact is concentrated in four critical decision domains where cost, risk and customer outcomes intersect.

1. Managing litigation risk from first contact

UK property and casualty (P&C) insurers are facing a growing litigation challenge. Legal costs across liability lines have been climbing steadily, fuelled by rising claimant solicitor activity, no-win no-fee arrangements and a legal environment that increasingly favours claimants.

The FCA has identified referral fees from claims management companies as a direct contributor to slower claims processing and rising costs. For P&C carriers, the difference between a claim that settles early and one that reaches court can be substantial.

In addition, UK carriers are now experiencing structural pressures that closely mirror the social inflation dynamics that have reshaped US liability markets. Evolving legal interpretations, increasing claimant awareness and rising expectations around compensation are driving higher settlement values across UK liability lines, reinforcing the need for early risk identification, consistent decision-making and proactive claims management.

For P&C carriers, the difference between a claim that settles early and one that reaches court can be substantial. By leveraging historical claims data, claimant characteristics, and early indicators of potential complexity, advanced analytics can highlight higher-risk cases at an early stage in the life cycle. This enables claims teams to prioritise effectively, allocate the appropriate expertise and manage the claim proactively. Intervening early enough can influence the trajectory of the claim and contain the overall cost.

2. Detecting fraud before it compounds

According to the ABI’s 2025 annual fraud report, UK insurers detected £1.16 billion in fraudulent general insurance claims in 2024, with organised crime rings active across motor, property and liability lines. Fraud doesn’t just impact insurers’ balance sheets; it drives premium increases, which place additional strain on policyholders already facing cost-of-living pressures.

Integrating advanced analytics with claims systems enables real-time fraud scoring at intake, drawing on anomaly detection, digital footprints, geospatial patterns and cross-referral to the Claims and Underwriting Exchange (CUE) database. Consider a motor liability claim at FNOL: a claimant matches a known solicitor referral pattern, CUE flags two prior claims in 18 months and the incident location is a recognised fraud hotspot. Analytics brings these disparate signals together in real time to generate a composite risk score that immediately routes the case to a specialist fraud-trained adjuster.

Early intervention can prevent unnecessary credit hire costs, inflated injury claims and legal escalation. The same dynamic exists across other lines of business, such as property, home and liability. Embedding advanced analytics early in the claims process allows insurers to act on those patterns immediately, preventing costs from escalating before they compound.

3. Sharpening reserve accuracy under inflationary pressure

Getting reserving right, both in terms of accuracy and timing, has become one of the most persistent challenges for UK claims teams. Inflationary pressure on labour, materials and supply chains has introduced significant volatility. Increasing claim volumes and complexity leave limited capacity for the detailed, case-by-case assessment that traditional reserving approaches depend on.

This challenge is especially visible in motor and property lines. In motor claims, evolving repair methodologies, part availability and credit hire costs can materially shift claim values over short periods. In property claims, rebuild costs influenced by regional contractor availability, weather-driven demand surges and inflated cost of materials can make early estimates quickly outdated. In both cases, initial reserve accuracy is critical, but it is inherently difficult to achieve using static or experience-based approaches alone.

By drawing on dynamic inputs like postcode-level risk data, historical claim development patterns, policyholder profiles, live weather feeds and current repair cost indices, predictive models can generate reserve estimates within hours of FNOL, continuously recalibrating as new information emerges. This not only improves consistency across handlers but also strengthens financial control by producing more reliable Incurred But Not Reported (IBNR) projections and reducing exposure to reserve volatility.

4. Smarter routing, faster resolution

Intelligent automation is changing how claims teams operate at every stage. Knowledge management tools give adjusters instant access to internal precedent, regulatory guidance and best practices, surfacing the right answer at the right moment. This is particularly significant for less experienced handlers who no longer need to wait on a senior colleague or work from incomplete knowledge.

Claims are sorted by complexity and urgency from the point of intake, with routine cases cleared quickly and those carrying litigation or severity flags directed to handlers best placed to manage them. In motor insurance, telematics and connected vehicle data are also increasingly feeding analytics models, providing objective insight into driver behaviour and accident dynamics at the point of claim notification.

Subrogation recovery presents a further opportunity that too few carriers are capturing systematically. Cases with recovery potential can be flagged at FNOL and directed accordingly, before the handling path closes off the opportunity. UK carriers applying predictive recovery analytics to their motor and property books have seen marked subrogation uplift, representing direct improvement to the loss ratio without additional claims volume.