The property and casualty (P&C) insurance industry is undergoing a fundamental transformation. Carriers are moving away from product-centric models — where each line of business is managed in isolation — and adopting a customer-centric architecture to better serve policyholders across their full risk profile and journey. This shift is not just about technology upgrades; it’s about reimagining how systems, processes, and products are designed to meet evolving customer expectations.

Several trends are accelerating this change: the demand for usage-based and event-driven products, the expansion of embedded distribution through APIs and ecosystems, and the need to unify offerings across lines of business for a seamless experience. According to McKinsey, P&C insurers that lead in customer experience outperformed their peers by 65 percentage points in total shareholder returns from 2017 to 2022. These CX leaders also saw stronger revenue and growth, lower expense ratios, and higher employee satisfaction, a clear signal that customer-centricity and performance go hand in hand.

Yet most insurers still operate with legacy constraints designed for product silos, not customer journeys. Their architecture tightly binds rules, workflows, and data to line-of-business-specific systems, limiting their ability to respond with speed and flexibility. As carriers adopt tools like underwriting workbenches, workflow orchestration layers, and rating platforms, it’s becoming clear that customer-centric architecture requires more than bolting modern tech onto outdated foundations — it requires a structural shift.

Why Shift to Customer-Centric Architecture?

While many insurers recognize the need to become more customer-aligned, their architecture tells a different story. Most still rely on systems built around products, not people, which limits their ability to move quickly, reuse components, or deliver unified experiences across channels.

In practice, this means underwriting logic is buried in core systems or spreadsheets, each line of business manages its own policy administration system (PAS), and digital tools often replicate rather than resolve existing silos. Channels are developed per product, resulting in a lack of shared services or an inconsistent customer journey. Even carriers who have invested extensively in their architecture and systems may lack the flexibility to share data, orchestrate personalized experiences, and adapt capabilities across lines of business.

This type of architectural approach wasn’t designed for today’s dynamic, customer-driven environment. In fact, 46.4% of insurers cite inflexibility to adapt to market changes as the most significant limitation of their current core systems. When every new product or update requires custom work per line of business, speed to market suffers — and so does the ability to meet rising customer expectations.

To stay competitive, insurers must stop building around the product and start building around the customer. And as technologies like generative AI (GenAI) become more deeply embedded in underwriting, this architectural shift becomes even more critical — because product-centric systems weren’t built to support the flexible, data-driven processes that GenAI demands.

Capabilities to Make Architecture a Strategic Enabler

The most critical shift doesn’t have to do with choosing the right tools; it’s about framing the architecture around supporting long-term agility, reuse, and growth. This means defining underwriting not as a system, but as a platform of capabilities.

To make this strategic shift, carriers must address three key architectural questions:

-

- What capabilities should be centralized? For example, product configuration, business rules, and workflow orchestration should be reusable across lines and channels.

- What should be decoupled from PAS? Functions like experience layers and rule engines must be abstracted to avoid one-off customizations for each product.

- What should underwriting own as a platform? Identify core services that underwriting needs to own — such as risk scoring, triage, and document intelligence — and design them for modularity.

Going through these questions and making operational changes can help insurers transition from siloed, PAS-bound processes to a flexible, platform-enabled operating model that can scale with evolving business and technology needs. Moving to a customer-centric architecture also empowers insurers to effectively integrate emerging technologies like GenAI and agentic AI to enhance their digital transformation efforts.

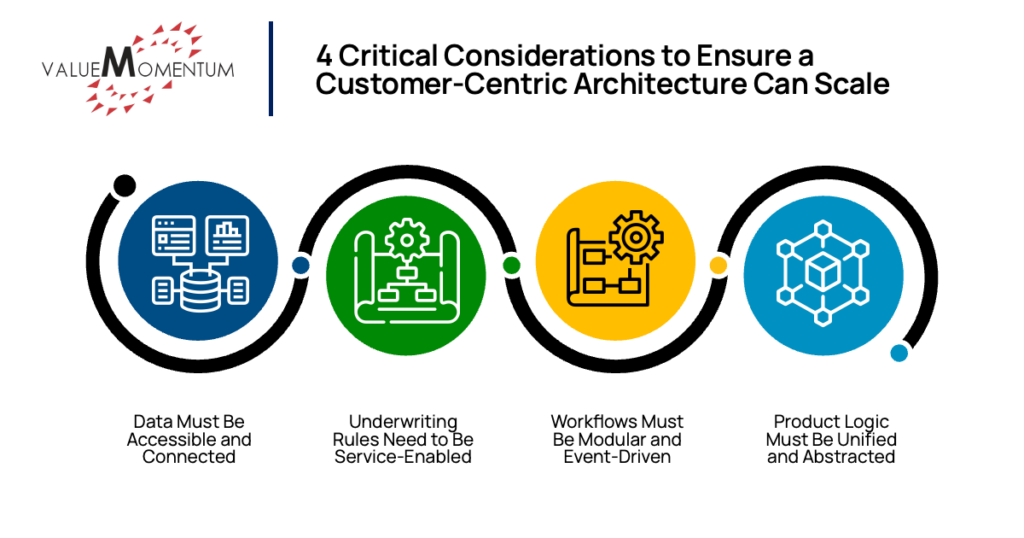

Here are four critical considerations to ensure a customer-centric architecture can scale alongside an insurer’s business needs:

- Data Must Be Accessible and Connected

To scale in the modern insurance industry, insurers must be poised to reap the full benefit of technology like GenAI and advanced analytics. AI models depend on both structured and unstructured data — not just policy data from the organization’s PAS, but also intake forms, inspection reports, and third-party sources. Siloed data limits GenAI’s potential. A unified data model and integration layer is essential.

- Underwriting Rules Need to Be Service-Enabled

Risk logic locked inside legacy portals or spreadsheets can’t support AI-driven decisioning, which prevents insurers from making improvements to their risk assessment or product recommendation capabilities. Underwriting rules must be externalized and made accessible via APIs to enable dynamic triage, scoring, and recommendations.

- Workflows Must Be Modular and Event-Driven

Rigid PAS workflows limit agility. However, carriers using modular workflows report faster product iterations and greater AI adoption due to reduced interdependencies across systems. These types of GenAI-powered, event-driven workflows allow orchestration of real-time processes such as document verification and provisional quoting, triggered by business events like submissions or exposure changes.

- Product Logic Must Be Unified and Abstracted

Product rules — such as rating logic, eligibility criteria, and forms configuration — should be maintained in a centralized, reusable service that is decoupled from any single line-of-business system. Centralizing product logic across lines of business and channels reduces duplication, ensures consistency, and supports cross-product comparisons, bundling, and tailored coverage recommendations.

When these foundational elements are in place, insurers can leverage a customer-centric architecture to reap the benefits of the latest tools and technology available. This approach makes capabilities like agentic AI and GenAI not just usable, but scalable and impactful.

Architecture as a Strategic Insurance Advantage

As P&C insurers look to modernize and grow, architecture is no longer just an IT concern — it’s a strategic business imperative. Customer-centric architecture enables carriers to move faster, scale smarter, and unlock the full value of emerging technologies like GenAI. It breaks down the silos that slow product innovation and replaces them with shared capabilities that serve the customer across every touchpoint.

Insurers that prioritize architectural flexibility, data accessibility, and platform thinking will be better positioned to adapt to market shifts, meet rising customer expectations, and build a future-ready foundation for underwriting. The time to rethink your architecture isn’t later: It’s now.

Find out how one insurer rethought its architecture to propel its business forward in our case study “Midwestern Specialty Insurer Optimizes Submission and Forms Process With Application Engineering.”