Insurers have made significant investments in core system transformations and tools like underwriting workbenches, yet many still struggle with launching or updating products across markets and channels. The problem isn’t the tools — it’s the fragmented architecture that underpins them.

Only 8% of insurers have successfully built connected underwriting platforms that are efficient, accurate, and improve the customer experience. Among these top performers, 70% have strong third-party data integration, compared to just 12% of their peers — highlighting the value of an aligned, modular architecture.

Most carriers still rely on hard-coded rules, workflows, and forms buried across legacy policy administration systems, spreadsheets, portals, and user interface (UI) layers. This makes reuse nearly impossible and introduces delays every time a product needs to be built, bundled, or extended. Operationalizing underwriting platforms means rethinking that structure so that tools work together and underwriting decisions scale with the business.

Rethinking Underwriting Platforms

Operationalizing underwriting platforms is less about picking the right technology and more about rethinking how core components — such as logic, workflows, data, and experiences — fit together. Many carriers are trying to define whether an underwriting platform should serve as an orchestration layer across policy admin systems, distribution channels, and product lines, or whether it should primarily enhance underwriter productivity and user experience.

A deeper challenge lies in determining how much business logic, which is often scattered across systems, should live inside tools like underwriting workbenches versus being externalized for reuse across the enterprise. With distribution ecosystems expanding to include brokers, digital APIs, managing general agents (MGAs), and embedded insurance channels, carriers are under pressure to support a diverse range of integrations.

But without abstraction or orchestration layers to isolate underwriting logic, every new integration requires custom development, hindering speed and driving up costs. Despite these external integrations and new tools providing insurers with a broader set of capabilities, layering modern tools on top of legacy systems may be increasing complexity rather than reducing it.

To truly transform underwriting, carriers must think platform-first, evaluating not only the tools available, but also the architecture and governance that tie them together.

Laying the Foundation for a Platform-Based Approach

There is no single blueprint for underwriting modernization. Every carrier operates with a unique combination of product strategy, distribution model, and technology footprint. What’s clear, however, is that legacy, product-centric architecture is becoming a constraint — limiting both speed to market and the ability to scale efficiently across lines and channels.

The real challenge isn’t just modernization: It’s alignment. Before carriers begin making architectural decisions, they must step back and evaluate the key factors that will define whether their underwriting platform can support long-term growth and agility.

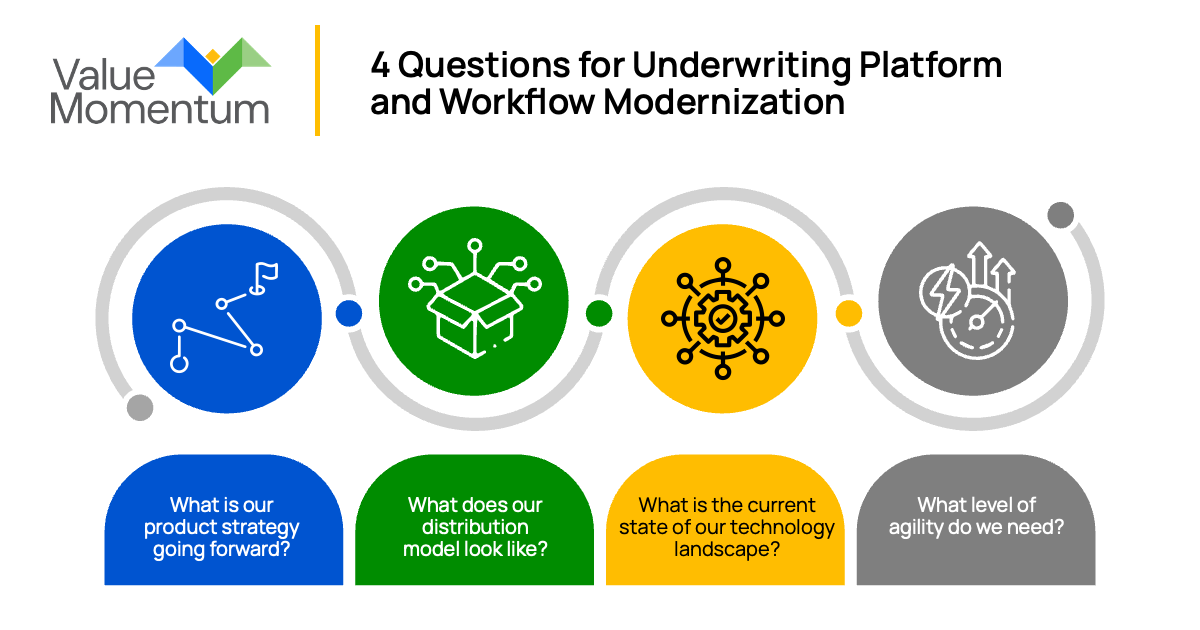

Here are four questions insurers must answer as they embark on modernizing their underwriting platforms and workflows:

1. What is our product strategy going forward?

The architecture required to support low-touch, high-volume personal lines looks very different from what’s needed for complex, manually underwritten commercial products. Carriers must assess whether they’re designing for modularity, product bundling, or usage-based models and choose an approach that aligns.

In fact, McKinsey predicts that by 2030, insurers that align their tools and architecture can automate pricing in simpler lines — like auto, personal liability, and home insurance — by over 90%, helping them scale efficiently and free up underwriters to focus on more complex risks.

2. What does our distribution model look like today — and tomorrow?

As insurers expand distribution through MGAs, broker APIs, embedded partnerships, and digital channels, their underwriting platforms must support that growth. The architecture should enable flexibility and reuse of core underwriting logic across channels, avoiding the need to rebuild for each new integration.

This means exposing services and decisions in a modular way, decoupling logic from any single front-end experience and designing for interoperability across ecosystems. Without this foundation, scaling distribution efforts will continue to introduce delays, duplicate effort, and inconsistent risk evaluation.

3. What is the current state of our technology landscape?

Many carriers already operate on multiple policy admin platforms and have adopted modern tools like underwriting workbenches, business process management engines, and low-code/no-code platforms. However, without a shared orchestration layer, these tools can create new silos, leading to process bottlenecks, duplicate logic, and inconsistent workflows across products and lines of business.

According to Deloitte, modernizing operating models by breaking down silos and aligning around customer and product needs enables carriers to respond faster to disruption, improve experiences, reduce costs, and support scalable growth. Without this shift, even well-intentioned investments in technology can slow the pace of business and create fragmented workflows that impact both customers and distribution partners.

4. What level of agility do we need?

For carriers expanding across geographies and partner segments, agility isn’t optional; it’s essential. In Hyland’s 2023 study, only 45% of insurers reported that they were strong or very strong in resilience and agility, while 37% noted that their organization was weak or very weak in this area. With nearly four in ten carriers struggling to adapt, it’s clear that traditional, siloed architectures are hindering businesses.

To avoid the trap of “rebuilding the wheel” with every update or new market entry, carriers must adopt an underwriting platform designed for continuous delivery, modular updates, and decentralized decision-making, ensuring speed, scale, and consistency.

These considerations aren’t just technical checkpoints — they’re strategic filters that help carriers determine how to align underwriting architecture with long-term business goals. Getting this clarity is the first step toward operationalizing an underwriting platform that can flex, scale, and deliver consistent value across the enterprise.

Underwriting as a Scalable, Strategic Platform

Modernizing underwriting isn’t about implementing the latest tools or chasing every new channel. It’s about building a connected, flexible architecture that establishes an underwriting platform — one that scales across products, distribution models, and partner ecosystems without constant reinvention.

The carriers that succeed won’t be the ones with the most tools, but the ones with the most aligned platforms. Underwriting, when operationalized the right way, becomes more than a process. It becomes a competitive advantage.

Want to find out more about how insurers are putting modern underwriting platforms to use? Read our case study Tokio Marine HCC – CPLG Creates World-Class Digital Distribution.