Claims costs across UK property and casualty (P&C) lines are rising, and litigation is accelerating the pressure. Compensation Recovery Unit data shows public liability claims up 15% year-on-year, from 57,372 to 65,950. Once a claim becomes a dispute, the costs go well beyond legal bills.

The FCA’s Consumer Duty raises the stakes further. A claim that drags on for months makes it very difficult to demonstrate good outcomes. AI-powered analytics can identify which claims are most likely to escalate at first notice of loss (FNOL), giving insurers the chance to intervene before costs build.

Why is the UK so exposed to litigation risk?

While litigation costs are rising across all markets, the UK faces specific pressures that make early prediction particularly important.

The biggest driver is social inflation, where litigation trends and claimant behaviour push costs up independently of the underlying cost of the claim. Third-party litigation funding, where outside investors finance legal cases for a share of the payout, is making it worse. Swiss Re’s 2024 analysis found social inflation contributed more than 10 percentage points to UK liability claims growth in 2023, with no signs of slowing down.

Large court awards set a precedent that future cases build on, making it progressively easier for claimants and their solicitors to push for bigger settlements. Because there is always a lag between when a policy is written and when a claim settles, the pressure already in the system continues to feed through.

The litigation risk problem

- High-cost concentration. A small fraction of litigated claims disproportionately inflate overall claims costs.

- Extended timelines. Litigation drives significant delays in claim resolution, increasing operational burden.

- Customer impact. Prolonged disputes erode trust, harming satisfaction and retention.

- Reactive detection. Litigation risk is often identified too late, limiting the ability to intervene.

What good risk management looks like

AI-powered litigation risk prediction changes how claims teams work, and the effects show up in several places at once.

High-risk claims are identified at FNOL and triaged to experienced handlers before claimant positions harden or legal representation escalates. Early intervention improves settlement outcomes, reduces claims leakage and shortens cycle times.

The operational impact is significant. Insurers using predictive litigation analytics have reported reductions in legal spend, improved reserve accuracy and faster resolution of complex claims.

Over time, these models also provide strategic portfolio insight. Patterns across claimant behaviour, injury types, regions and legal representation become visible earlier, helping claims leaders refine reserving, pricing and defence strategies across the book.

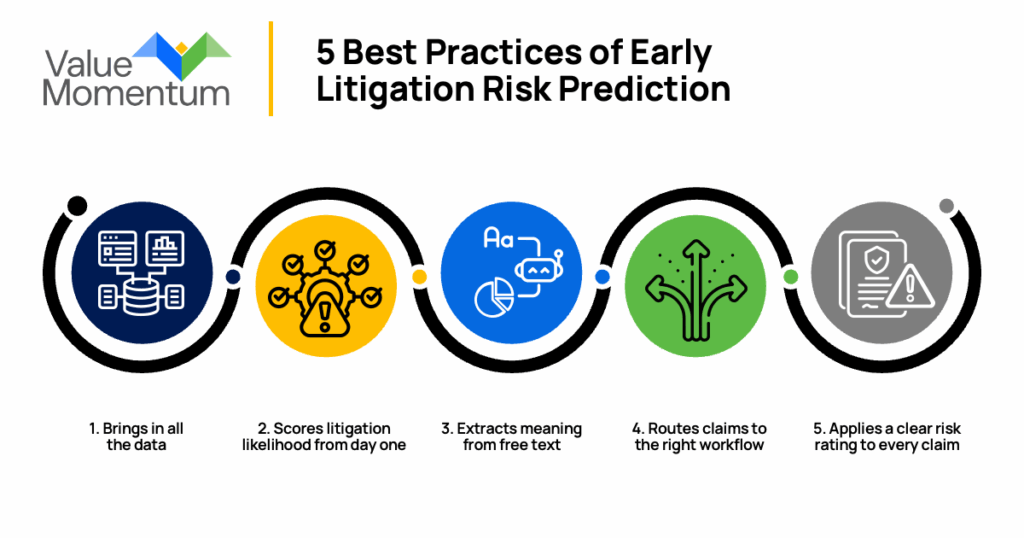

Early litigation risk prediction: 5 best practices

Investing in early risk prediction is one of the highest-return decisions a claims operation can make. Here is what a system that delivers results looks like in practice.

- Brings in all the data. A strong prediction system draws on both structured data, such as claim history, injury type, geography and legal representation, and unstructured sources including adjuster notes, call transcripts and claimant narratives. Structured data tells you what happened. Unstructured data often tells you where things are heading.

- Scores litigation likelihood from day one. Using patterns from historical claims, the system produces a litigation propensity score at FNOL. That score is not static. It updates as new information comes in throughout the life of the claim, so the team always has a current read on risk.

- Extracts meaning from free text. Natural language processing lets the system read adjuster notes and call transcripts and pick up on sentiment, dispute signals and claimant intent. These are the early warning signs that experienced handlers develop an instinct for over years. A good system surfaces them consistently, across every claim, from day one.

- Routes claims to the right workflow. Claims are grouped by complexity, severity and financial exposure and directed accordingly. Straightforward claims move quickly through automated pathways. Higher-risk files get flagged for specialist attention before costs build.

- Applies a clear risk rating to every claim. The system produces a litigation risk index for each claim. High-risk claims go straight to legal counsel or senior adjusters. Moderate-risk claims are monitored with targeted flags. Low-risk claims follow the standard process without unnecessary handling.

The bottom line

Over the next decade, insurers need more than stronger legal panels to stay ahead of litigation costs. Organisations need to identify escalation risk early, intervene proactively and operationalise litigation intelligence across the claims life cycle.

In an environment shaped by social inflation, Consumer Duty expectations and increasing claims complexity, early litigation prediction is quickly becoming a core claims capability rather than a competitive advantage.

AI-driven litigation prediction allows claims teams to detect behavioural, procedural and contextual signals much earlier in the claims journey, enabling faster triage, earlier engagement and more informed intervention strategies. The result is not only lower legal and indemnity costs, but also improved customer outcomes, reduced claims leakage, better reserve management and greater consistency in claims handling decisions across the portfolio.

To learn more about how insurers are navigating the impact of litigation risk, read ValueMomentum’s whitepaper “Combating Social Inflation: Strategies for Claims Organizations to Reduce Leakage.”