Insurers have gotten more comfortable incorporating artificial intelligence (AI) into their workflows in recent years, and the number of carriers that have deployed some form of AI is only growing. But as organizations are shifting from solely traditional AI to generative AI in insurance, many leaders are trying to navigate how this technology can best help them grow.

Traditional AI has helped property and casualty insurers analyze their existing data to make predictions about future outcomes, automate processes, and improve decision-making capabilities. This typically occurs in the form of machine learning models, rules-based systems, or algorithms designed for a specific task. Traditional AI tools can help with more accurate risk assessment and pricing, smoother processing of routine claims, and better fraud detection.

But unlike traditional AI, generative AI can not only analyze existing patterns, it can also generate new data that mimics the patterns it has been trained on. Tools like ChatGPT have come into the forefront because of the text, visual imagery, and sounds they can generate based on users’ prompts. When applied to different use cases across the insurance value chain, generative AI holds untold potential to improve operational efficiency, streamline claims management, and serve as a co-pilot for underwriters, among other possible uses.

Applying Generative AI in Insurance

Because of its ability to generate increasingly complex output when trained effectively, generative AI holds broad promise across the value chain, from underwriting to claims to distribution. If insurers train their generative AI tools on enough data and provide specific prompts to finetune the output, generative AI can help them approach products, experiences, and operational processes in new ways to sustain a competitive edge.

Insurers just beginning to leverage generative AI in their workflows may not be sure where to apply the technology to get the most value. Here are a few ways to get started with generative AI across the entire insurance value chain.

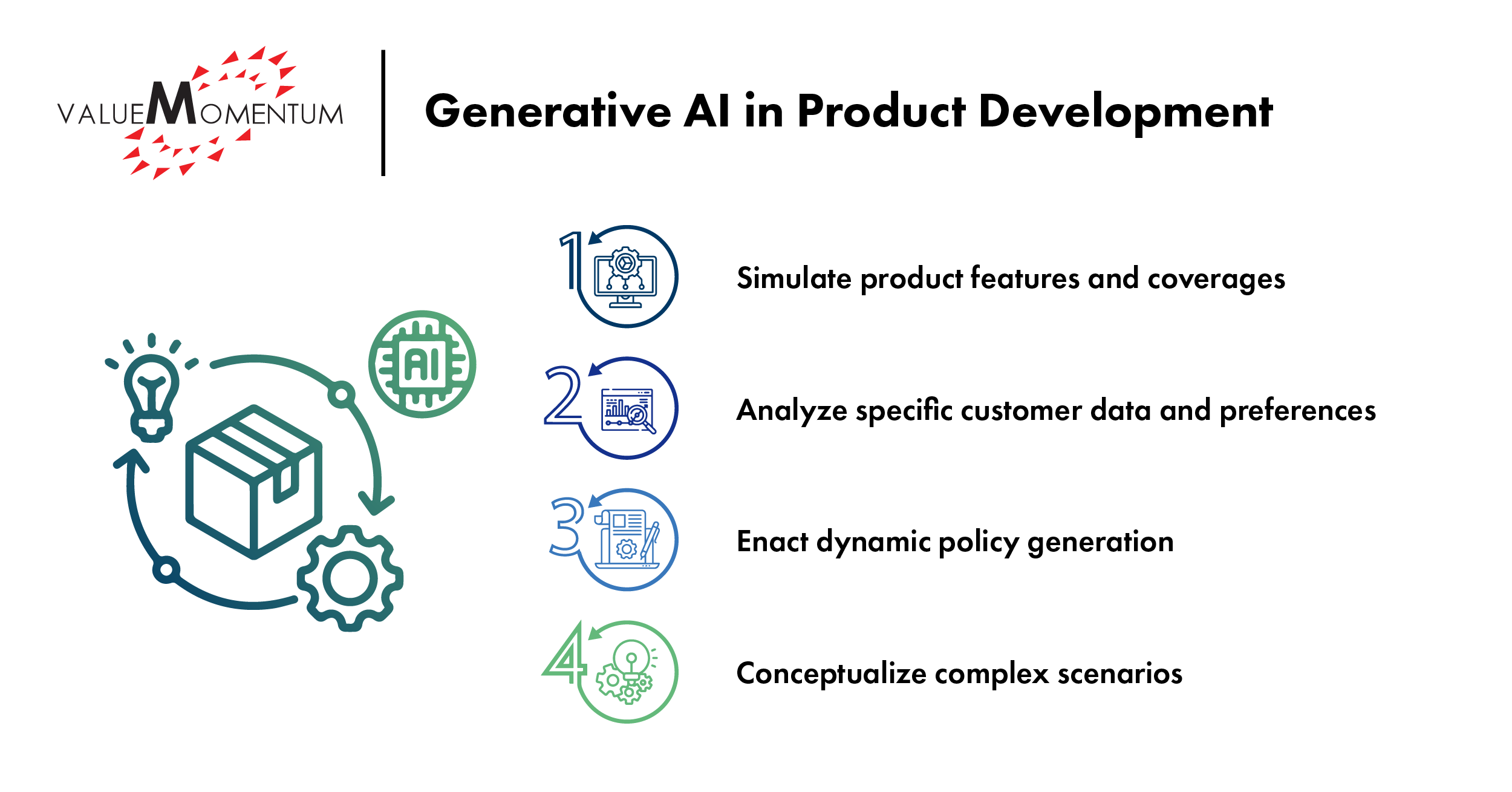

Product Development

Carriers have used traditional AI to optimize their product offerings based on historical data about the market. But generative AI can help insurers change the way they conceive of their products beyond just the historical data.

Insurers can apply generative design techniques to simulate innovative product features and coverages, offering a broader range of options than traditional product design methods. Similarly, generative AI can analyze specific customer data and preferences to create tailored products for individual customers or niches, taking segmentation another step further. Insurers can also enact dynamic policy generation to offer real-time coverage adjustments that adapt based on changes to an insured’s circumstances or risk profile.

Generative AI’s ability to conceptualize more complex scenarios can also enable insurers to embark on more robust scenario simulation for emerging risks like cyber and climate change to allow carriers to know their products are meeting evolving customer concerns. Other aspects of customer experience can also be augmented by leveraging interactive content and simulations to help policyholders understand the coverage provided by newer insurance products.

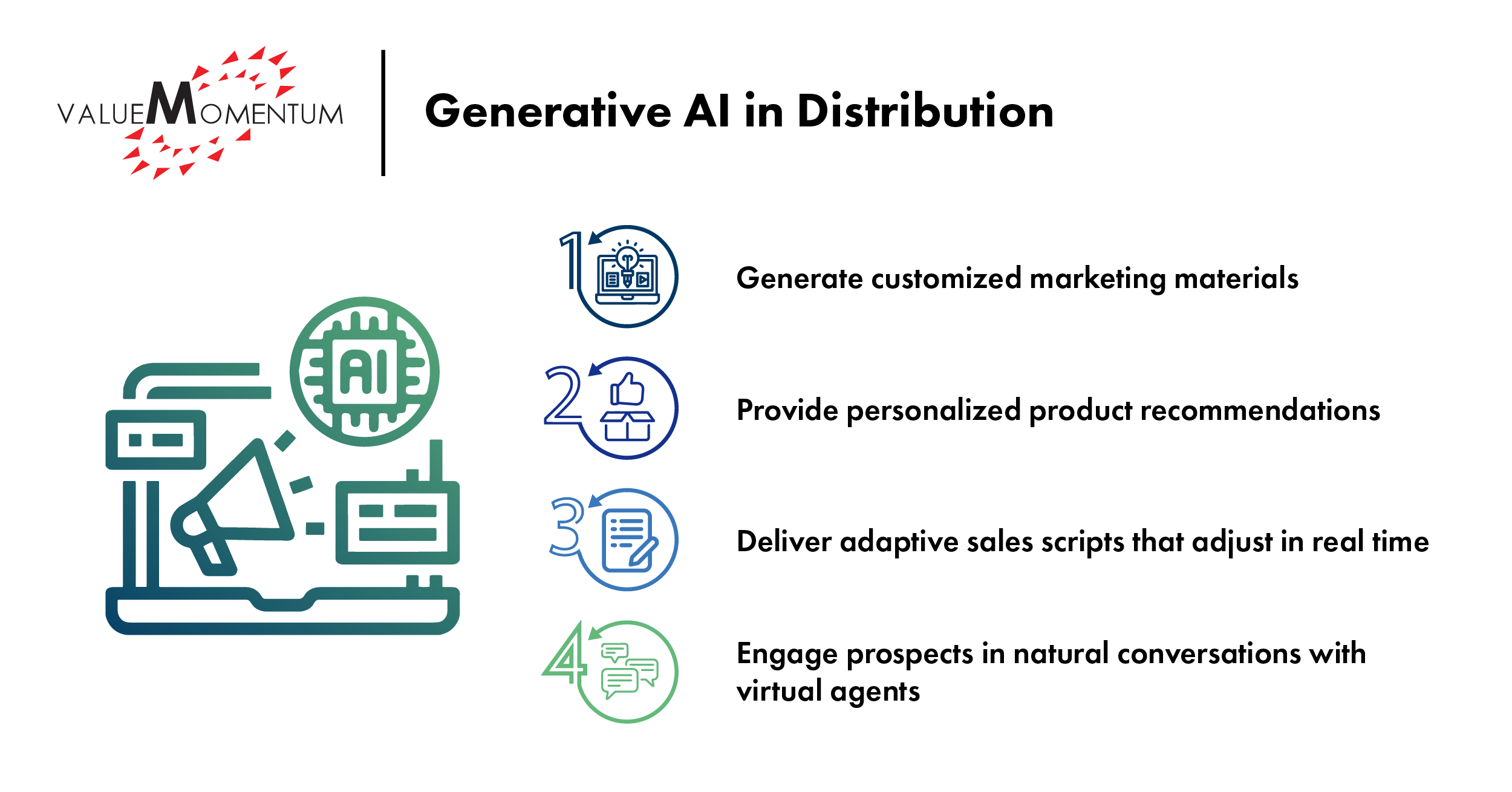

Distribution

Traditional forms of AI have helped insurers improve the efficiency of their distribution processes. But leveraging generative AI can not only help insurers simulate multiple types of distribution strategies under various market conditions, but it can also help deliver truly personalized customer experiences.

It can generate customized marketing materials from emails to social media posts to web content that is tailored to individual customers or segments. In addition, generative AI tools rooted in deep learning capabilities can provide highly personalized product recommendations based on specific customers’ unique needs and preferences, elevating personalization beyond basic segmentation.

Generative AI can also improve the way agents and brokers serve policyholders and prospects, delivering adaptive sales scripts that adjust their messaging in real time based on customer interactions and feedback. Virtual sales agents can also be improved by incorporating generative AI; virtual agents powered by higher forms of AI can have more natural conversations with prospects, guiding them through their product options and the buying process in a highly personalized way.

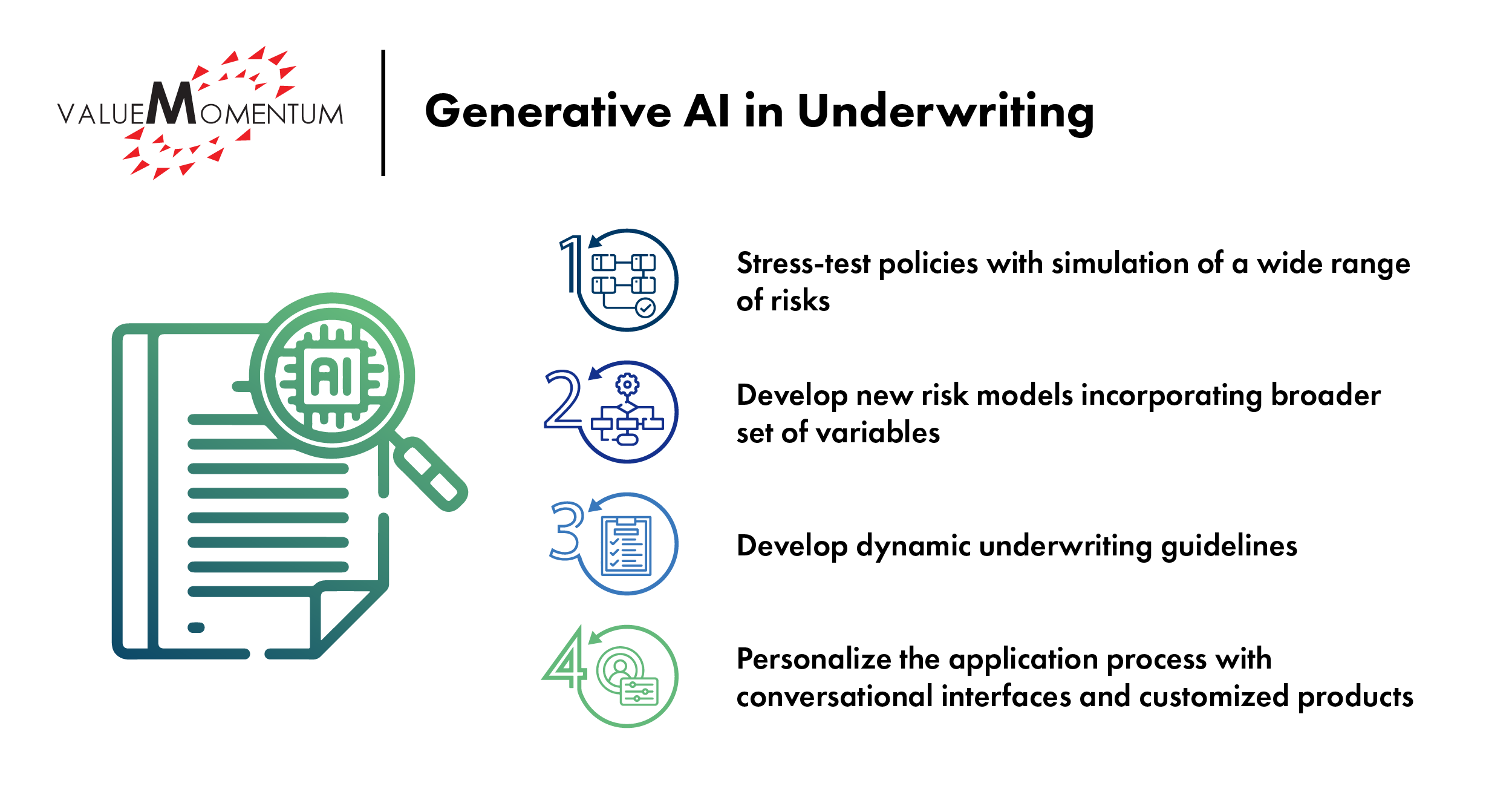

Underwriting

Traditional AI has helped insurers improve their underwriting processes by handling tasks such as automating risk assessment, helping forecast potential claims based on a policyholder’s profile, and flagging potential fraud cases against known patterns. None of these use cases for traditional AI should be replaced by generative AI; instead, generative AI should be applied in complementary ways to optimize the underwriting process for an insurer.

As noted for distribution and product design, generative AI can simulate a wide range of scenarios. For underwriting, this means a broader simulation of risk types, including rare and emerging risks, to help insurers stress-test their policies under various conditions. Generative AI can even develop new risk models to incorporate a broader set of variables like latent risk factors and emerging trends to offer a more comprehensive analysis.

On top of enhanced risk assessment, generative AI can also help carriers develop dynamic underwriting guidelines that adapt to changing risk landscapes, improving their responsiveness to shifts in the market. Tools with generative AI at the root can help personalize the application process with more conversational interfaces and highly customized insurance products for niche markets or individual customers.

Claims Management

Claims is a vital customer touchpoint where insurers can differentiate their experience to stand out amongst the competition. Carriers have applied traditional AI to claims to automate parts of the process and improve efficiency, but the potential of generative AI offers new opportunities to enhance claims assessment, derive more detailed predictive insights, and hone personalization efforts.

Generative AI can create synthetic yet realistic data sets that train fraud detection models without involving sensitive data. It can also be used along with augmented reality to provide interactive, highly detailed damage assessments that can help adjusters visualize damage more accurately to provide better cost estimates.

The claims management process can also benefit from having generative AI predict future claims volumes and complexity, enabling insurers to allocate resources and adjust workforce levels in anticipation of claim surges like those after a natural disaster. Insurers can also use generative AI to improve claims handling and settlement negotiation. Not only can it simulate settlement negotiation scenarios to speed up claims resolution time and arrive at optimal settlement amounts, but it can also generate customized communication strategies for each claimant to deliver a truly personalized claims process.

Moving Forward With Generative AI

Insurers should not think of generative AI as a replacement for the traditional AI methods already incorporated into their workflows but rather as a complementary technology. Leveraging both types of technology can help carriers build out a modern tech stack to help them improve efficiency across the entire value chain and deliver more value for their customers.

While claims, underwriting, distribution, and product development can all benefit from adding generative AI into the process, there is also opportunity to improve overall operations, increase developer productivity and testing capabilities, and enhance customer experiences across the board.

To learn more about driving business success across the value chain with modern technology, check out ValueMomentum’s whitepaper Driving Business Value With Insurance Data Analytics.