Most commercial carriers manage their product content manually. Their product teams have to interpret large standard content manuals, track frequent circular updates, and translate that content into everything from rating logic to coverage and rules definitions and forms across multiple states and product lines. But manual approaches to aligning with industry-standard content cannot keep up with how fast things change.

According to RegEd, state-level insurance regulatory changes were already up more than 13% through mid-2025 compared to the same period in 2024 — and federal actions are expected to accelerate further, cascading additional requirements down to states. Across the industry, interpretation varies across products, teams, and states; updates are deferred; and workarounds accumulate.

A streamlined approach to insurance policy content management addresses each of these pressure points, enabling carriers to launch and update products faster, automate complex rating and compliance logic, and simplify maintenance across states and markets.

Why Product Content Management Breaks Down

While product teams are aware of the need to update industry content as regulations change or new circulars are released, many have not implemented a standardized approach.

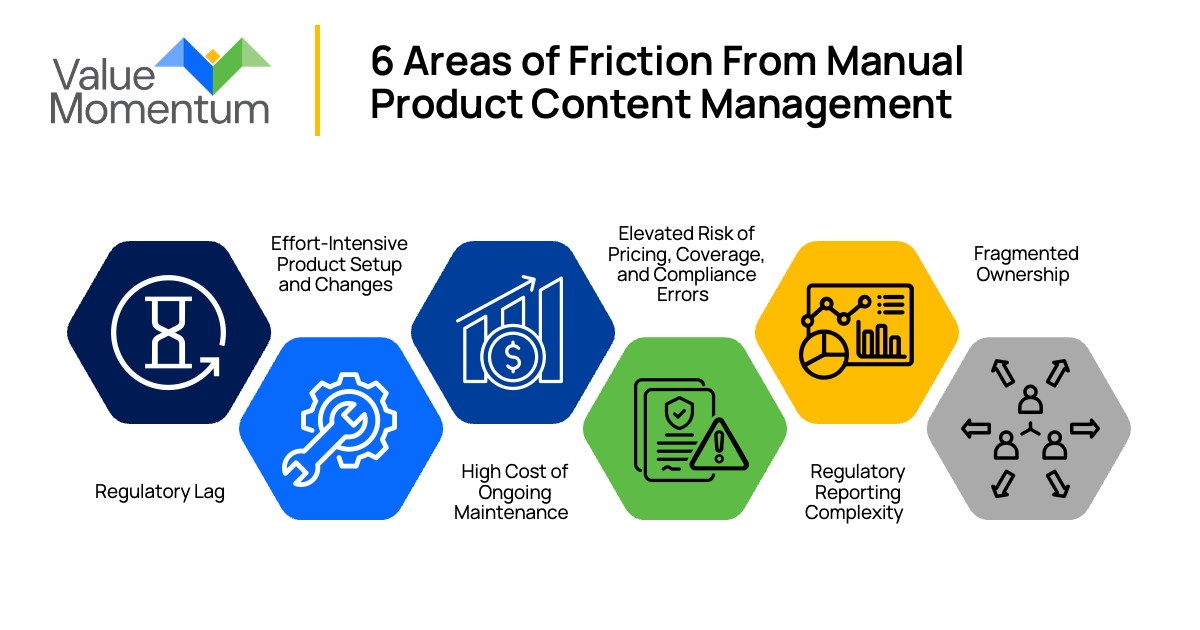

Here are six ways that manual product content management processes are creating friction in the day-to-day work of product teams:

1. Regulatory Lag

Circulars are frequently deferred due to overlapping business priorities, leaving many carriers operating multiple update cycles behind current bureau content. Missed or delayed regulatory adoption increases audit findings, regulatory fines, corrective action plans, and state Department of Insurance scrutiny. It can also make remediation effort greater and create reputational risk that is difficult to quantify until it surfaces during a market conduct exam.

2. Effort-Intensive Product Setup and Changes

Every standard content change triggers a cascade of manual work: reconfiguring coverages, updating rules, revising forms, and validating rating logic, followed by extensive regression testing before anything reaches production. This leads to longer release cycles, higher defect rates, and slower speed to market when expanding into new states or launching new products.

3. High Cost of Ongoing Maintenance

Actuarial and IT teams in most commercial lines organizations spend a disproportionate amount of time on maintenance instead of on strategic activities. Advanced pricing analysis, portfolio optimization, and modernization initiatives all take a back seat to keeping existing products current, leaving carriers slower to adapt at precisely the moment the market demands more agility.

4. Elevated Risk of Pricing, Coverage, and Compliance Errors

Manual product content management introduces misalignment between rating logic, underwriting rules, and policy forms, which only gets worse over time. The downstream consequences range from incorrect premiums, outdated policy forms, and coverage gaps to increased disputes, leakage, and combined ratio volatility.

5. Regulatory Reporting Complexity

Non-standard product definitions create friction at every regulatory checkpoint. Manual reconciliation is required to meet reporting standards, and the effort involved increases with each deviation introduced into the product model. This causes increased scrutiny during market conduct exams, additional audit and correction cycles, and a reactive compliance posture.

6. Fragmented Ownership

Product configuration, compliance testing, and regulatory filing are typically owned by different teams, with no single point of accountability. Decisions move slowly. Rework is common. And when something goes wrong, identifying where the breakdown occurred — and who is responsible for fixing it — takes longer than it should.

Individually, each of these challenges is manageable. But combined, they take up an increasing share of organizational capacity, leaving carriers less prepared for the evolving regulatory environment and less agile to adapt to market opportunities.

Business Benefits of a Streamlined Approach

These pain points are the byproduct of a product content management process that was built for a lower volume and slower pace of regulatory change. A streamlined approach enables carriers to launch new products and roll out updates significantly faster — reducing the manual interpretation and configuration work that currently stretches release cycles.

Analysis of rating, forms, pricing, and compliance changes as well as the impact on the current portfolio can be streamlined with automation, along with the IT effort involved in these changes. Maintenance across products, states, and markets becomes simpler and more repeatable, and regulatory changes can be absorbed as routine rather than as a disruption to ongoing operations.

And the benefits of a streamlined approach extend across the organization. Product and underwriting teams can keep products standardized and up to date without constant rework. Actuarial and pricing teams can recover capacity consumed by manual circular analysis and regression testing and redirect their bandwidth to advanced pricing work and portfolio optimization. Compliance and regulatory teams gain the end-to-end traceability that market conduct exams demand.

Enabling a governed, repeatable model for product content management turns regulatory updates into an ongoing operational discipline, ensuring that carriers can evolve their product portfolio with the speed needed to stay ahead in a competitive landscape. This goes for rolling out new lines of business or expanding into additional regions with differing product requirements.

Product Content Management as a Strategic Investment

The regulatory environment commercial lines carriers are dealing with is not static, and the operational consequences of managing product content manually are becoming harder to absorb. As compliance gaps widen and the competitive need for product innovation and state expansion grows, a scalable, governed process for product content management is an investment in business agility.

Effective product content management is not merely a technology problem. It is an operational discipline that requires clear ownership, repeatable processes, and an infrastructure that keeps up with an increasingly complex regulatory environment.

To learn more about taking a strategic approach to product design and management, visit our Product Strategy services page.