In the face of escalating losses, catastrophe (CAT) risks are no longer just a concern for property and casualty (P&C) insurers — they are a defining factor in underwriting performance and portfolio profitability. In 2024, global insured losses from natural CATs hit $137B, with projections pointing to $145B in 2025. Much of this is driven by secondary perils such as severe convective storms, floods, and wildfires. Meanwhile, emerging threats such as cyber risk are gaining momentum, with global cybercrime expected to cost $13.8T annually by 2028.

This isn’t a passing trend. The last decade (2015-2024) has been the warmest on record, and natural CAT events are becoming more frequent, more intense, and harder to predict. In 2023, the US P&C market recorded a staggering $24.6B underwriting loss — the highest in a decade. With an average combined ratio just over 100 in the past 10 years, CAT events alone contributed around 8 points.

To stay ahead, insurers are moving beyond traditional methods. They are building more resilient CAT operating models, enhancing data pipelines, and developing specialized capabilities. CAT modeling is no longer a technical necessity; it’s a strategic imperative for managing volatility, improving underwriting accuracy, and driving sustainable growth.

Understanding Catastrophe Risk: Materiality and Maturity

The first step for insurers is to assess how material CAT risk is to their overall enterprise risk — and how mature their CAT modeling function is in supporting that risk. Then carrier organizations need to identify capability gaps and make targeted interventions.

Lloyd’s principles offer a useful framework for evaluating maturity levels and identifying gaps to align with materiality. Insurers are expected to manage CAT exposure in line with their risk appetite and tolerance as well as leverage effective tools to support efficient exposure data capture, management, and use. A risk-based framework should be used to quantify and monitor exposure.

On top of this, it is critical to have the teams and expertise needed for both business and strategic needs. It is also essential to have a well-defined and well-maintained view of CAT risk. Finally, insurers need to ensure they have built a robust governance function that includes strong oversight of risk aggregations.

Modeling Catastrophe Risk: Challenges and Opportunities

However, bridging these gaps is not without its challenges. While CAT modeling has long been central to risk management for P&C insurers, building a truly mature function requires more than just running models. As risks evolve and underwriting pressures mount, insurers must adopt a more integrated and strategic approach.

Key challenges to this shift include:

- Operating model dilemma: Should you build an in-house team, outsource to brokers or vendors, or adopt a hybrid model? The right choice depends on the organization’s business strategy, access to expertise, cost-quality-time tradeoffs, and the level of control needed.

- Talent constraints: CAT modelers are a rare breed. In the US, they are outnumbered roughly 5:1 by actuaries, 25:1 by underwriters, and 125:1 by sales agents. India, due to its strong STEM talent pool and various historical factors, has emerged as a global hub for CAT modeling.

- Exposure data quality: Incomplete or inaccurate property and location data can skew loss estimates. Accurate address geocoding and risk coding as well as inclusion of key secondary modifiers enhance the quality of results greatly. Third-party data cleansing tools and property data products are available to enrich exposure data.

- Model limitations: All models are simplifications, and each comes with its own assumptions, uncertainties, and blind spots. Knowing when and how to use a model — and when not to — is just as important as the model itself. Model evaluation is key to ensure the model is truly fit for purpose, but it requires deep domain knowledge and experience.

- Analytics-driven decisions: CAT modeling should be part of a broader analytics strategy, integrated with internal and external data, spatial and advanced analytics, and automation and business intelligence (BI) tools to support real-time underwriting and risk management decisions.

- Value-chain integration: CAT modeling must extend beyond the reinsurance function and become embedded across pricing, underwriting, exposure management, capital modeling, and risk transfer. This requires a robust technology and data infrastructure.

The Toolkit for Successful Catastrophe Modeling

Maximizing the value of CAT modeling isn’t just about running better models — it’s about embedding the right capabilities across the entire insurance value chain.

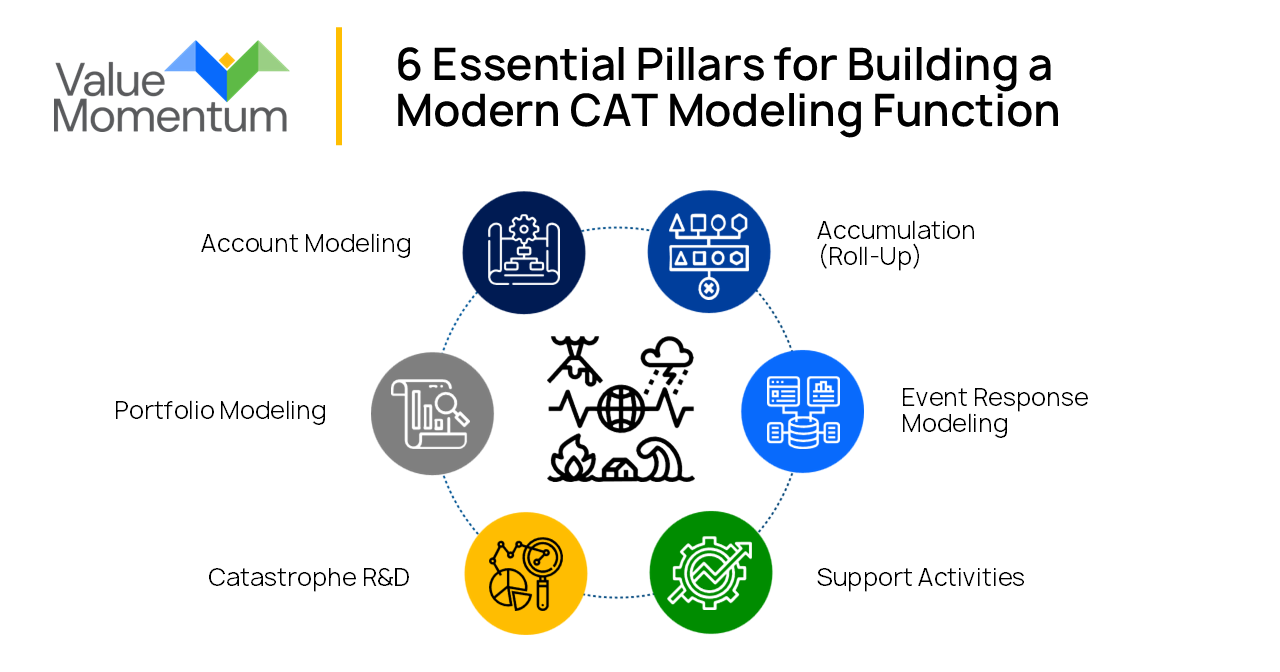

Here are six essential pillars for building a modern CAT modeling function:

1. Account Modeling

Apply CAT models at the underwriting level to support smarter risk selection and pricing. It may not always be prudent to evaluate every account, but insurers can focus on complex, high-value, or high-risk accounts to balance operational efficiency with deep insights.

2. Accumulation (Roll-up)

Insurers can understand their total exposure through the aggregation of individual risks. A mature CAT risk function allows a comprehensive and segmented view of exposure and loss across the enterprise on a quarterly basis, if not more frequently. An efficient accumulation process supporting real-time exposure monitoring and control serves as the backbone of advanced exposure management.

3. Portfolio Modeling

Use CAT models to create and analyze portfolios by geography, peril, product, and business unit. CAT modeling plays a critical role in portfolio optimization processes. The results of portfolio modeling are used in exposure management and underwriting strategies. When modeled with reinsurance programs, they support risk and capital management as well as compliance requirements, such as stress and scenario tests.

4. Event Response Modeling

During live events like hurricanes or wildfires, CAT modeling helps estimate incurred-but-not-reported (IBNR) losses, allocate resources, and guide policyholder communications. A strong event response capability transforms modeling from a back-office tool into a frontline advantage.

5. Catastrophe R&D

Own your risk. Develop a proprietary “CAT view of risk” tailored to your organization’s specific risk profile and loss experience. Rather than relying solely on vendor models, this internalized view allows insurers to calibrate loss results and layer in proprietary insights on climate trends, emerging risks, societal/economic trends, and more. It all begins with the evaluation and validation of vendor models.

6. Support Activities

Invest in data enrichment, spatial and advanced analytics, automation, a modern IT infrastructure, and BI tools. Statement of value (SOV) cleansing, coding, and validation is a critical activity for reliable results. Since CAT risk is location-dependent, spatial analytics play a major role in deriving insights into exposure concentrations, loss distributions, and loss drivers. These capabilities enable consistent, high-quality assessments and pave the way for AI-powered risk scoring and dynamic pricing.

Together, these pillars define what it takes to build a modern, resilient CAT modeling function. As risks grow more complex and data becomes more abundant, leaders in this space will be those who know how to turn data into action and models into strategic assets.

Strategic Enablement: Preparing for the Future

To truly thrive in a volatile risk landscape, insurers must embed CAT modeling into core workflows — not silo it within actuarial or reinsurance functions. When integrated across the organization, CAT modeling becomes a strategic enabler, informing everything from underwriting to capital deployment.

Achieving this level of integration requires more than software licenses or outsourced services. It demands high-quality location intelligence, fit-for-purpose models, skilled resources, and a robust operating model for insight consumption.

Often, it also means rethinking how talent and tools are sourced — blending in-house knowledge with specialized partners to scale effectively. When done right, CAT modeling does more than help insurers survive disruption; it helps lead them through it.

Want to learn more? Explore our Catastrophe Modeling and Risk Management Services to discover best practices for CAT risk assessment and mitigation in an increasingly unpredictable world.