Insurers know cloud transformation is a necessary part of modernization, yet many are still in the early stages of their journey. Migrating legacy systems onto the cloud is costly, time-consuming, and risky due to the complexity of these platforms. Concerns about data privacy, security, and meeting compliance only compound these factors.

As a middle ground, many insurers are operating on a hybrid model to get the most out of the investments they have already made in their on-prem infrastructure while also offering the more streamlined, modern experience cloud-based systems can offer. But even insurers with hybrid infrastructures can maximize the value of their cloud investments with continuous, holistic monitoring of both on-premises and cloud platforms.

Traditional monitoring tools have focused on individual system components rather than providing a unified view of an insurer’s entire infrastructure. To ensure operational efficiency, security, and performance, insurers must shift from fragmented monitoring tools to a unified observability approach that provides real-time insights across all environments.

The Business Impact of Unified Observability

Not only does unified observability help reduce downtime and accelerate claims processing by detecting and resolving problems faster, but it also enhances risk assessment and pricing decisions by giving underwriters comprehensive visibility.

In addition, unified cloud observability strengthens fraud detection and streamlines claims management through real-time insights into anomalies and suspicious activity as well as optimizes IT spending and maximizes ROI through predictive analytics on resource utilization, cloud costs, and IT investments. Real-time API monitoring can also enhance sales performance and digital distribution capabilities.

However, many insurers struggle with implementing unified observability due to technical and operational challenges. Understanding these obstacles is key to developing a successful strategy.

There are four key challenges to keep in mind during implementation:

- Fragmented data and inconsistent visibility. Data is often siloed between different sources, analyzed on various tools, and monitored by separate teams without having a view into the infrastructure as a whole.

- High volume and variety of data and tools. The sheer amount of telemetry data generated across cloud and on-premises environments creates challenges in data flow, integration, and analysis.

- Tracing issues in microservices and containerized architectures. While these architectures enhance agility and scalability for insurers, they also make end-to-end tracing complex.

- High volume of alerts and notifications. If alerts lack context and prioritization, critical issues may be missed while teams chase false positives or minor errors.

Overcoming these challenges requires more than just tools — it demands strong capabilities that enable insurers to gain real-time visibility, streamline their data management, and improve their incident response.

One client we worked with has already seen improvements to operational efficiency across its claims and underwriting functions. Standardizing its processes around metrics and consolidating its observability tools has provided a holistic view of its environment that is enabling the insurer to conduct business better.

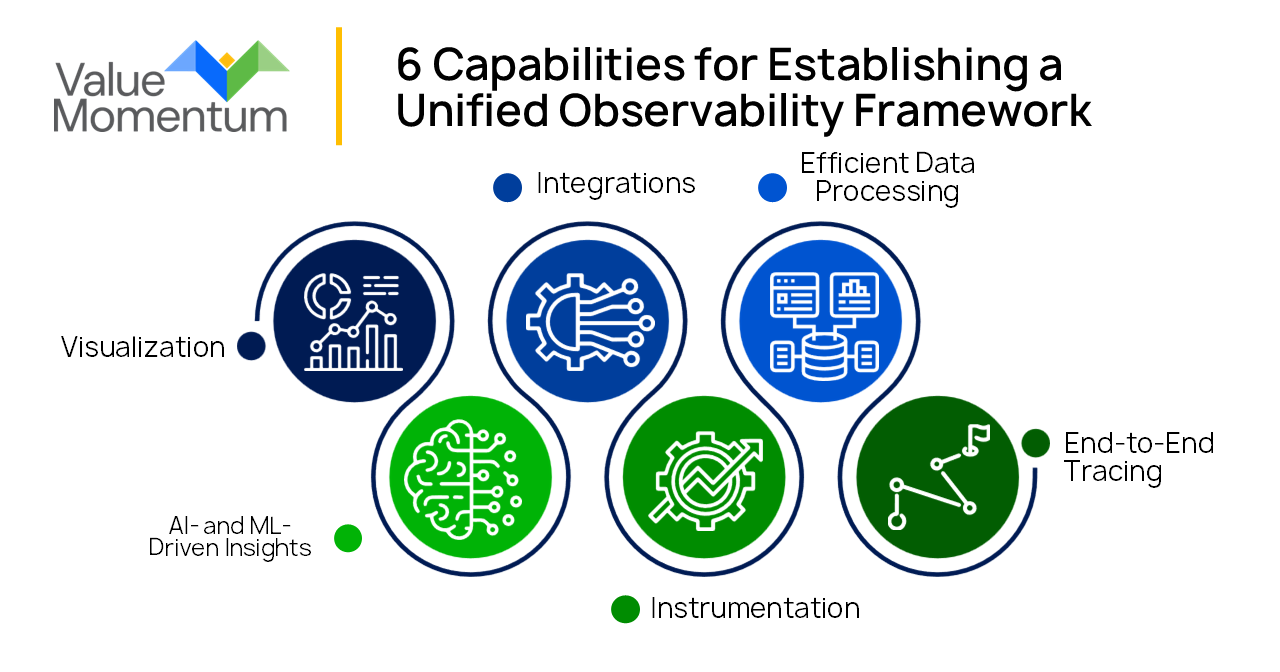

6 Capabilities for Establishing a Unified Observability Framework

To effectively implement unified observability, insurers must adopt a framework built on six key capabilities.

1. Visualization

Insurers need customizable dashboards, reports, and visualizations tailored to each team, including developers, operations, business leaders, and customer support. These tools should prioritize real-time digital experience monitoring (DEM), which is essential for evaluating the performance and availability of digital services from the end-user perspective.

By analyzing customer interactions across platforms, insurers can use visualization with DEM to reduce friction that could impact policyholders and agents.

2. AI- and ML-Driven Insights

Artificial intelligence (AI) and machine learning (ML) play a critical role in identifying performance anomalies, predicting system failures, and automating root cause analysis. These capabilities allow insurers to proactively address potential issues before they disrupt operations.

By leveraging AI-powered observability, insurers can detect early warning signs of outages before they impact claims processing, underwriting, or customer portals; automate anomaly detection to highlight irregular patterns in transaction processing or system health; and reduce manual troubleshooting by using automated root-cause analysis to pinpoint issues faster and enable self-healing mechanisms.

3. Integrations

A unified observability framework must seamlessly integrate with existing IT ecosystems, such as incident management systems, notification channels, and self-healing services. These integrations ensure observability data triggers automated workflows to resolve issues efficiently.

For example, integrating observability with IT service management (ITSM) tools can automatically create tickets for critical incidents, reducing manual intervention and response time.

4. Instrumentation

To collect telemetry data across applications and infrastructure, insurers need automatic instrumentation via software development kits, libraries, or agents. Reducing reliance on manual instrumentation lowers insurers’ development overhead while maintaining deep system visibility.

While automatic instrumentation captures standard performance metrics, insurers should use manual instrumentation selectively for custom business logic tracking, such as fraud detection algorithms or policy underwriting workflows, and deep-dive performance tuning when auto-instrumentation doesn’t support a specific programming language or framework.

5. Efficient Data Processing

Insurers generate massive amounts of telemetry data from various sources, like applications, databases, cloud services, and APIs.

To manage this effectively, a centralized observability platform should aggregate multiple telemetry sources in a structured, standardized format; autoscale storage and processing based on demand to prevent resource bottlenecks; and optimize cost models to guarantee that observability tools scale efficiently without excessive infrastructure spending.

6. End-to-End Tracing

To fully understand how transactions and requests flow across distributed systems, insurers need end-to-end tracing. Distributed tracing allows teams to visualize the journey of an application request across microservices, APIs, and cloud environments, pinpointing bottlenecks or failures.

However, distributed tracing is not the same as dynamic tracing. While distributed tracing tracks requests end-to-end, dynamic tracing provides in-depth diagnostic information about code execution. Insurers should differentiate these capabilities and use them appropriately to gain both high-level system insights and granular troubleshooting data.

These capabilities form the foundation for real-time insights, automated issue resolution, and seamless digital interactions, ensuring insurers stay competitive in an increasingly cloud-driven world.

Unlocking the Full Potential of Cloud Investments

As insurers continue their cloud transformation journey, unified observability is no longer a luxury — it’s a necessity for ensuring system reliability, operational efficiency, and seamless digital experiences. This strategic investment not only improves system performance and reduces downtime but also positions insurers to adapt to future challenges, meet evolving customer expectations, and maintain a competitive edge.

To learn more about how investing in cloud platforms helps insurers drive business growth, read our case study “Erie Insurance Optimizes Data Operations With MarkLogic Enterprise Data Hub on AWS.”